Investing

Activate Your Equity Income

Global Equity Enhanced Income Fund

Delivering an equity income portfolio can often result in a tug-of-war between income, capital growth and a balanced portfolio. The Allspring Global Equity Enhanced Income (GEEI) Fund has been designed to overcome this challenge.

What

Equity income myth busters

Think you know equity income? Sophie Scott, head of International Portfolio Specialists, clears up three myths and how GEEI seeks to address them head-on.

Read more

Transcript

Sophie Scott: It’s true. Dividends aren’t guaranteed like bond coupons, but that doesn't make them unreliable. Companies work really hard to maintain their dividends. They signal financial strength and investor confidence. Even during rare disruptions like the 2020 pandemic, most companies resumed their payouts quickly. To focus on a consistent income, we look beyond simply chasing dividends. We systematically identify fundamentally attractive companies with healthy cash flows, solid margins, and sustainable payout policies. We monitor seasonality and market conditions, and we add an options overlay to top up our income. Together, these levers help us deliver a steady and reliable income stream.

Income stocks are typically companies with stable business models and stable earnings—great for dividends, but capital growth can be modest. On the other hand, growth stocks typically reinvest their earnings to fuel expansion. This means typically no dividends but higher, long-term capital growth. The good news: With intentional design, it's possible to build a portfolio to generate capital growth and reliable income. By investing a small amount of the portfolio in non-dividend-paying stocks and managing beta to be in line with the benchmark, it’s possible to capture upside and deliver a reliable income in one portfolio.

Depending on its design, a global equity income portfolio can differ quite a lot from a traditional global equity portfolio—often underweight tech, the U.S., and growth and overweight areas such as the U.K., staples, and value. These imbalances can cause performance outcomes to differ from expectations. We don't think that income should come at the expense of capital growth or diversification. By maintaining a globally diversified portfolio, carefully managing sector and region exposures as well as style risk, we aim to deliver a balanced portfolio that is designed to deliver consistent returns over time.

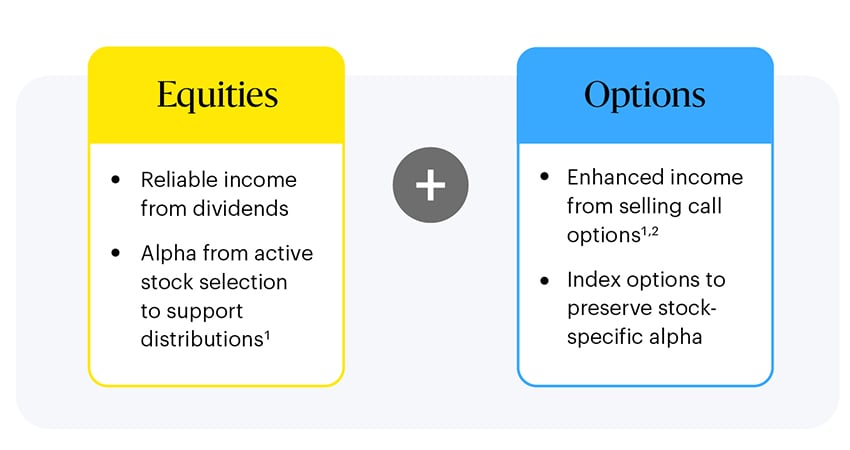

Targeting high, consistent income plus access to the growth potential of global equities

Enhanced income

Targets a high, consistent yield—6% p.a. (paid monthly)*

Growth potential

Designed to capture the long-term growth potential of global equities

Balanced exposures

Helps mitigate style swings with a global portfolio diversified across factors, regions and sectors

*As of 31 March 2026. A target is indicative only, is not guaranteed and does not take into account fees or charges that will reduce returns.

A diversified approach to income delivery

1The fund intends to make consistent monthly income distributions. Capital gains from both equity and option portfolios can be utilized in addition to equity dividends to achieve the target distribution. 2Only partial potential upside is given up in order to preserve long term capital growth.

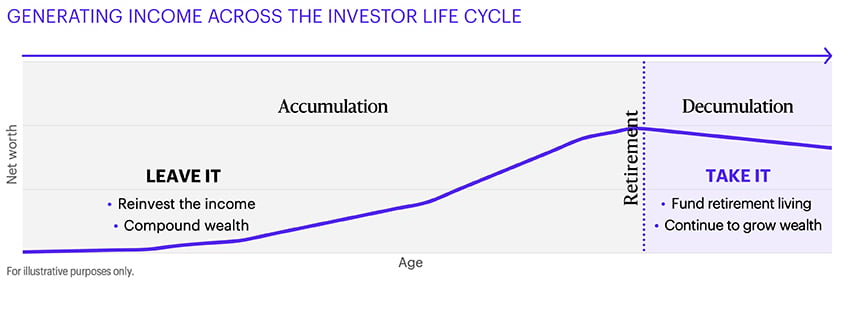

Take it or leave it: receive regular income or reinvest for long-term growth

To learn more, download the paper here.

Why global equities for income and capital growth?

01.

Global opportunity set

Avoid concentration risk with a diversified portfolio

02.

Long-term capital growth

Income investors also need to grow their assets

03.

Robust real returns

Help overcome the impact of inflation

High dividend equities deliver robust capital growth in excess of inflation.

Breadth of quantitative tools and fundamental validation combined with an actively managed options overlay

A monthly distributing fund targeting 6% per annum*

For more insight into the fund, including recent distributions and performance, read our product sheet.

*As of 31 December 2025. A target is indicative only, is not guaranteed and does not take into account fees or charges that will reduce returns.

Learn more about the fund:

Visit the fund page for performance, deeper investment details and fund documents.

Featured insights

Check out our insights and perspectives.

Global equities are a key part of long-term investing. Blending passive and systematic active global equity strategies may help investors efficiently navigate changing market conditions and enhance long-term investment outcomes.

Sophie Scott, head of International Portfolio Specialists, breaks down the three strategic pillars behind the Allspring Global Equity Enhanced Income (GEEI) Fund and how they work together to deliver a powerful equity income solution.

Investor needs shift over time. Our Global Equity Enhanced Income (GEEI) strategy is designed to meet near-term and long-term goals by providing consistent income plus growth in a diversified global equity portfolio.

Insight

The Three Rs of RetirementConventional wisdom encourages retirees to de-risk portfolios, but we believe equities remain essential. Our approach to equity in retirement is built on three principles: take more risk, focus on real returns, and demand reliable income.

Wai Lee’s approach to solving investment challenges is embedded in his three principles of research. It all started with engineering school and a Mercedes-Benz V-6 engine.

Key risks

Smaller-company securities risk: securities of companies with smaller market capitalisations tend to be more volatile and less liquid than securities of larger companies.

Geographic concentration risk: investments concentrated in specific geographic regions and markets may be subject to greater volatility due to economic downturns and other factors affecting the specific geographic regions.

Global investment risk: securities of certain jurisdictions may experience more rapid and extreme changes in value and may be affected by uncertainties such as international political developments, currency fluctuations and other developments in the laws and regulations of countries in which an investment may be made.

ESG risk: applying an ESG screen for security selection may result in lost opportunity in a security or industry, resulting in possible underperformance relative to peers. ESG screens are dependent on third-party data, and errors in the data may result in the incorrect inclusion or exclusion of a security.

Currency risk: currency exchange rates may fluctuate significantly over short periods of time and can be affected unpredictably by intervention (or the failure to intervene) by relevant governments or central banks or by currency controls or political developments.

Emerging market risk: emerging markets may be more sensitive than more mature markets to a variety of economic factors and may be less liquid than markets in the developed world.

Equity securities risk: these securities fluctuate in value and price in response to factors impacting the issuer of the security as well as general market, economic and political conditions.

Leverage risk: the use of certain types of financial derivative instruments may create leverage which may increase share price volatility.