Beatles, Bonds, and the Taxman

Allspring’s tax-free-man, Ken Jacob, portfolio specialist with the Municipal Fixed Income team—and former radio disc jockey—explains why municipal bonds may strike the right chord for investors seeking tax-free income, attractive yields, and a way to keep more of what they earn.

Authors

-

Ken Jacob

7/8/2026

4 min read

Topic

Municipal Bonds

Key takeaways

- Tax-exempt income stands out: Elevated yields and tax advantages may make municipal bonds a compelling source of after-tax income.

- Today’s backdrop appears favorable: Higher rates have historically created attractive entry points, with improved return potential and more manageable rate sensitivity.

- Active matters in municipals: Careful credit selection and sector positioning can help investors identify opportunities and manage risks in a complex market.

From playlists to tax planning

I was a radio disc jockey in college back in the 1990s, when terrestrial radio was still a thing and actual humans chose what went on the air. We had a fair amount of creative freedom, and timely themes often drove my song choices.

As a penny-pinching, money-conscious undergrad, my playlists took on a clear theme as tax season approached. Songs by some of my favorite artists lamenting the negative impact of taxes made it into my rotation.

Tracks like the Beatles’ “Taxman,” Cheap Trick’s “Taxman, Mr. Thief,” and the Steve Miller Band’s “Take the Money and Run” were staples that time of year.

Back then, I spent far more time curating playlists than thinking about taxes. Today, however, like many investors, minimizing my tax bill is a high priority—not just during tax season, but year-round.

Tax-exempt income

One of the best ways investors can help shield their income from taxes is by investing in tax-exempt municipal bonds. Municipal bond interest is generally exempt from federal income taxes and, in many cases, state and local taxes as well. The tax‑equivalent yield of municipal bonds often exceeds that of taxable bonds, corporate credit, and even some equity dividend strategies.

The higher rate environment that we’ve been in over the past year has made tax-exempt income from municipals even more attractive. This can be especially appealing to high‑income, high-tax investors.

For example, a municipal bond or mutual fund yielding 4% currently offers a taxable-equivalent yield of more than 6% for an investor in the highest federal tax bracket. That’s more than a 50% increase in net income when compared with a taxable equivalent.

Exhibit 1: Yield comparison

| Yield to worst (YTW) | Tax equivalent YTW* | |

| Bloomberg Municipal Index | 3.67% | 6.20% |

| Bloomberg Municipal AAA Index | 3.53% | 5.96% |

| Bloomberg Municipal BAA Index | 4.48% | 7.57% |

| Bloomberg High Yield Municipal Index | 5.53% | 9.34% |

| Bloomberg US Aggregate Bond Index | 4.67% | 4.67% |

| Bloomberg US Corporate Index | 5.13% | 5.13% |

Sources: Bloomberg Finance L.P. and Allspring. *Based on the highest federal (37%) and state tax bracket and assuming the investor is also subject to the additional 3.8% Medicare surtax on net investment income (40.8%). Assumes non-deductibility of state income tax at federal level. As of 29-May-26.

Historically high yields

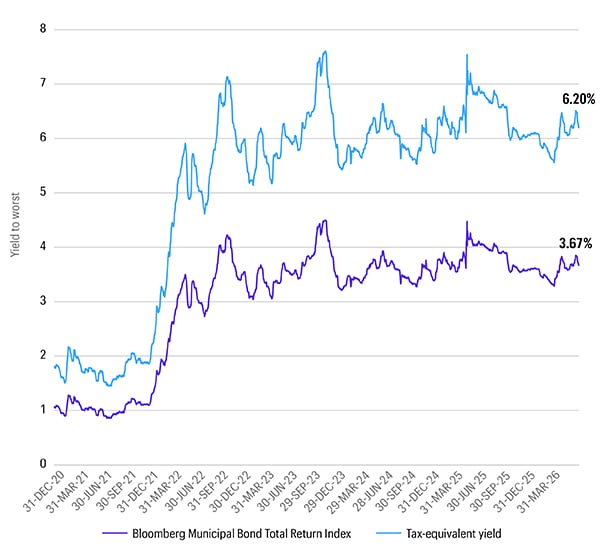

Yields are also trading near historical highs, which makes municipals more attractive than they have been in recent memory.

Municipal bond yields continue to look attractive. Yields stood at just 0.95% in January 2021, before rising through 2022 and peaking at 4.49% in October 2023 as the Federal Reserve raised interest rates. While yields have moderated some lately, they continue to look attractive, particularly on a tax-equivalent basis.

Exhibit 2: Muni yields over time

Sources: Tax Foundation and Allspring. *Based on the highest federal (37%) and state tax bracket and assuming the investor is also subject to the additional 3.8% Medicare surtax on net investment income. Assumes non-deductibility of state income tax at federal level. As of 29-May-26.

Reduced relative risk potential

Additionally, municipal bonds have historically exhibited relatively low credit risk. Compared with corporate bonds, municipals have experienced lower default rates across all credit ratings. For example, BBB-rated municipal bonds have historically had lower default rates than AAA-rated corporate bonds.

Exhibit 3: Comparative default rates for municipal and corporate debt

| MUNICIPAL (%) | CORPORATE (%) | |

| AAA | 0.00 | 1.10 |

| AA | 0.04 | 1.34 |

| A | 0.13 | 2.39 |

| BBB | 0.96 | 5.34 |

| BB | 5.07 | 16.26 |

| B | 10.84 | 27.63 |

| CCC/C3 | 37.80 | 57.70 |

| Investment-grade | 0.22 | 3.31 |

| Speculative-grade | 8.32 | 25.46 |

Sources: Bloomberg Finance L.P. and Allspring, as of 31-Dec-25. Source: S&P Global Ratings. For municipal defaults, S&P’s study period was 01-Jan-86 to 31-Dec-24 (dated 06-May-25). For corporate defaults, S&P’s study period was 01-Jan-81 to 31-Dec-24 (dated 29-April-25). The calculation represents a 15-year cumulative default rate. S&P’s study calculations include all ratings in the C category, from CCC to C.

Municipal bonds also can be an important part of a well-diversified portfolio. Municipals historically exhibit lower correlation to equities1 compared with corporate bonds, and with stable cash flow, they can also offset volatility in other asset classes. In higher rate environments, municipals can serve as both a portfolio ballast and volatility dampener.

A compelling backdrop

Periods of higher interest rates have historically created favorable entry points for municipal bond investors. Elevated tax-exempt yields can help enhance total return potential; reduce interest rate sensitivity; and, alongside strong credit fundamentals, appeal to income-focused, tax-aware investors.

Active management may help investors capitalize on this environment. In our view, disciplined credit selection remains essential and experienced managers can identify relative value across sectors, seeking to select bonds thoughtfully based on price and opportunity.

Related insights

It seems like everyone wants to talk about space right now. But Allspring’s Head of Municipal Fixed Income, Nick Venditti, would rather talk about the roads, hospitals, and water systems that keep our world running—and the municipal bonds behind them.

Nick Venditti gives a recap of 2025's municipal bond market before diving right into 2026. He calls for investors to consider longer-maturity municipal bonds and look to active management for opportunity amid volatility.

1. Source: Bloomberg Finance L.P.

Bloomberg Municipal Bond Index

The Bloomberg Municipal Bond Index is an unmanaged index composed of long-term tax-exempt bonds with a minimum credit rating of Baa. You cannot invest directly in an index.

Bloomberg Municipal AAA Index

The Bloomberg Municipal AAA Index measures the U.S. municipal tax-exempt AAA rated bond market. It includes general obligation and revenue bonds, which both can be pre-refunded years later and get reclassified as such. You cannot invest directly in an index.

Bloomberg Municipal BAA Index

The Bloomberg Municipal BAA Index measures the U.S. municipal tax-exempt BAA rated bond market. It includes general obligation and revenue bonds, which both can be pre-refunded years later and get reclassified as such. You cannot invest directly in an index.

Bloomberg High Yield Municipal Bond Index

The Bloomberg High Yield Municipal Bond Index measures the non-investment-grade and nonrated U.S. dollar–denominated, fixed-rate, tax-exempt bond market within the 50 United States and four other qualifying regions (Washington, D.C.; Puerto Rico; Guam; and the Virgin Islands). The index allows state and local general obligation, revenue, insured, and prerefunded bonds; however, historically the index has been composed of mostly revenue bonds. You cannot invest directly in an index.

Bloomberg U.S. Aggregate Bond Index

The Bloomberg U.S. Aggregate Bond Index is a broad-based benchmark that measures the investment-grade, U.S.-dollar-denominated, fixed-rate taxable bond market, including Treasuries, government-related and corporate securities, mortgage-backed securities (agency fixed-rate and hybrid adjustable-rate mortgage pass-throughs), asset-backed securities, and commercial mortgage-backed securities. You cannot invest directly in an index.

Bloomberg U.S. Corporate Index

The Bloomberg US Corporate Bond Index measures the investment grade, fixed-rate, taxable corporate bond market. It includes USD denominated securities publicly issued by US and non-US industrial, utility and financial issuers. You cannot invest directly in an index.

All investing involves risks, including the possible loss of principal. There can be no assurance that any investment strategy will be successful. Investments fluctuate with changes in market and economic conditions and in different environments due to numerous factors, some of which may be unpredictable. Each asset class has its own risk and return characteristics.

This material is provided for informational purposes only and is intended for retail distribution in the United States.

Diversification does not ensure or guarantee better performance and cannot eliminate the risk of investment losses.

Standard & Poor’s, Fitch Ratings, and Kroll Bond Rating Agency rate the creditworthiness of bonds from AAA (highest) to D (lowest). Ratings from AA to CCC may be modified by the addition of a plus (+) or minus (-) sign to show relative standing within the rating categories. Moody’s rates the creditworthiness of bonds from Aaa (highest) to C (lowest). Ratings Aa to Caa may be modified by the addition of a number 1 (highest) to 3 (lowest) to show relative standing within the ratings categories. Credit quality and credit-quality ratings are subject to change.

ALL-06302026-p20sfwn5