Climate Transition: Burning Questions for the Next Phase

Henrietta Pacquement, Allspring’s head of Sustainability, discusses climate-transition investing and key points for investors to consider as they move toward the next phase of the climate transition.

Key takeaways

- Investors are more sophisticated in how they approach sustainability, including how they combine financial and climate goals and how they evaluate benchmark choices.

- Increased weather volatility has had negative effects on supply chains and gross domestic product, and is an important consideration for asset values of firms.

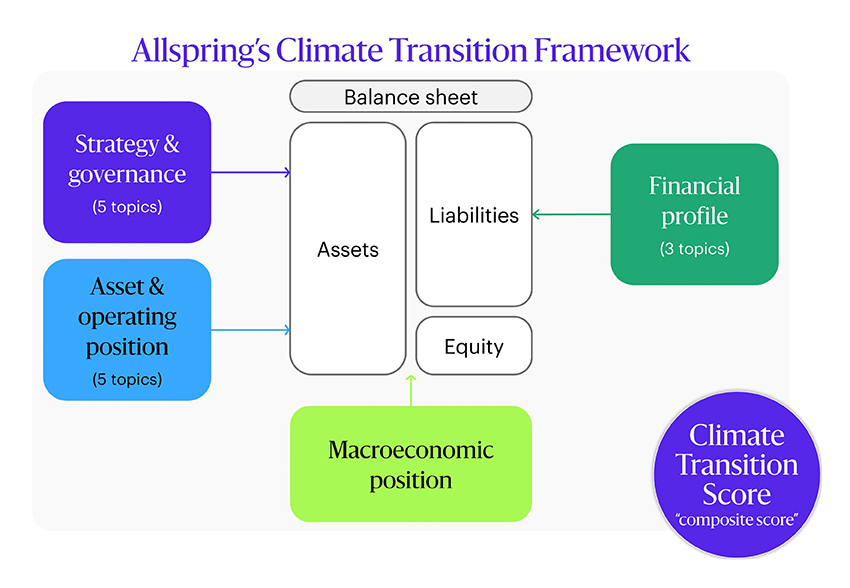

- Allspring’s climate framework combines proprietary, company, and third-party data to help identify firms that are leading on climate transition from those that are lagging.

Transitioning the global economy to net-zero emissions is a decades-long process with wide-ranging implications for virtually every industry. That translates to enormous opportunities. Savvy investors will consider how investment dynamics change over the transition period, along with the availability of company data, the precision of metrics, and the evolution of the regulatory environment.

As a follow-up to last year’s “Climate Transition: Burning Questions for Credit Strategies,” Henrietta Pacquement, head of Sustainability, shared her views and Allspring’s focus on climate-transition investing at a recent investment industry event. This article summarizes key points for investors as we move toward the next phase of climate-transition investing.

Where is sustainable investing at currently and where is it going?

Practically speaking, there’s been huge progress among asset managers integrating sustainability characteristics. That can be in terms of portfolio management, engaging with companies, or making day-to-day operations more sustainable. I'd say it's a mix overall, but there's been a lot of progress across the investment industry, including bringing sustainability themes in house.

Allspring’s philosophy and investment approach is forward looking, and we see a lot of reasons to be optimistic and opportunistic. It’s important to understand the current state, but we invest for the future with a framework that integrates financial outcomes with sustainability results.

How are investor views toward sustainability evolving?

We're seeing increased sophistication in terms of the approach to sustainability. Investors are realizing they can achieve financial goals while incorporating climate considerations. That includes more sustainability themes in portfolios. We're getting a lot of interest from clients who are looking at some of their traditional benchmarks and portfolios and asking, “What can I do to express sustainability themes?” Climate is a big theme in that context. They often have already done a lot of work on the equity side and are now looking more closely at their fixed income portfolios. Some are examining their duration exposure and yield profiles and projecting where they want to be. As they plan that transition, many investors are also thinking about how to incorporate climate goals in the fixed income space.

Another question we frequently hear from clients is, “Which benchmark should I use?” Conventional wisdom may point to a specialized climate-focused index, but our research shows that a standard fixed income index is often better suited to benchmark a climate-transition strategy. Starting with a broad market index and building the portfolio with thorough, forward-looking analysis offers greater flexibility without restricting sustainability and investment performance. On the other hand, specialized climate benchmarks mechanically exclude sectors and companies based on backward-looking information, which can obstruct both climate efforts and performance going forward. The index landscape is growing, and we’ll continue to evaluate benefits of the various benchmark options.

Education is essential. Investors need to know what it means to incorporate sustainability and to decide how they want to express their views in their portfolios.

Education is essential. Investors need to know what it means to incorporate sustainability and to decide how they want to express their views in their portfolios.

What does it mean to integrate climate transition in a portfolio, and why is it becoming more commonplace?

We see climate as a source of both risk and return that should be considered alongside all other performance factors. That means evaluating risk and return with an eye to both climate’s physical effects, such as floods and droughts, as well as strategic and competitive effects like decarbonization’s impact on markets and geopolitics. In the summer and fall of 2023, climate change plus El Nino conditions caused the Rhine River to fall to depths well below what’s required for normal commercial barge traffic. Then in December, the river was closed because water levels were too high, making it unsafe for ships to pass under bridges. Weather volatility is having measurable, negative effects on supply chains and gross domestic product. These dynamics aren’t exclusive to Europe. Rivers around the world are showing distress, including the Amazon, Mississippi, Nile, and Yangtze. We believe asset managers should consider future interruptions like these when evaluating supply chain efficiency and the asset values of firms.

Climate change also has competitive and geopolitical ramifications. Take Europe’s pivot away from Russian gas. Geopolitics forced Europe to quickly turn to liquified natural gas imports from the U.S. and elsewhere while accelerating the development of renewable energy. That was spurred in part by low-cost wind and solar components from China. But is Europe replacing energy dependency on Russia with dependency on equipment from China and natural gas from the U.S.? This may be true in part, but we believe Europe’s pivot is very positive in financial terms and is a big win for decarbonization. Natural gas comes from a much broader, geopolitically stable supply base than the European pipeline gas. And while China is a cost leader in renewables, many other nations supply wind and solar components at increasingly competitive prices. Bottom line? While the analysis is nuanced, we believe Europe’s energy economy is better positioned today than it was five years ago.

What is Allspring’s decision framework for integrating climate transition into portfolios?

The transition to net-zero emissions touches virtually every aspect of the economy. We take an inclusive approach, so we’re looking across sectors to build our portfolios. We don’t rely on exclusions, which we think is quite a blunt process. Fixed income has a huge role to play to fund the change needed.

Our Climate Transition Framework is a valuable tool in our fundamental analysis and portfolio construction. The framework identifies a broad range of risks and opportunities that might affect a company’s competitiveness, including:

We combine proprietary technology and data with company data and third-party data to assess a company’s climate-related risks and opportunities alongside other investment factors. Our fundamental approach includes determining where a company is in their climate journey. Historical data can tell us where a company is coming from, but we need to know where the company is going. Doing this work from a bottom-up perspective is crucial in how we look to distinguish companies that are leading on climate transition from those that are lagging in decarbonizing the real economy.

How do you view the regulatory environment?

Increased regulations are improving company disclosures. That helps asset managers gain a better understanding of what's really going on at those firms, and it helps investors better understand what’s in the funds they're investing in. That’s even the case in some of the more difficult geographies such as the U.S., which is grappling with the scope of regulations regarding company disclosures. Greater access to data and more consistent disclosure requirements are especially important as sustainability strategies develop and are increasingly global in scope.

Interoperability is key here to bridge the gap among different sets of regulatory standards and frameworks around the world. The Task Force on Climate-related Financial Disclosures (TCFD) is one of the initiatives in this area. Allspring’s inaugural 2023 TCFD report covers a range of information about our climate-related efforts—from our climate governance structure to the metrics and targets we use for relevant strategies.

What are some of the recent developments you’ve seen in Asia?

Depending on the country or region, there are different levels of interest and progress on sustainability. I’m encouraged that in my own recent trips to Asia I’ve gotten more questions on sustainability—a notable pickup from conversations in the past. Education is essential. Investors need to know what it means to incorporate sustainability and to decide how they want to express their views in their portfolios. And that varies, which requires some customization.

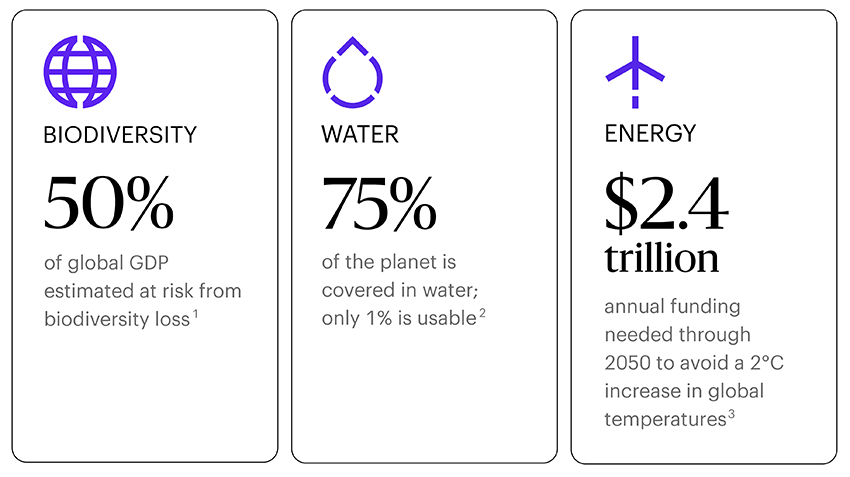

The types of themes talked about are evolving as well. Climate is a big topic. That’s sometimes driven by regulators looking at it in a very holistic way across all of their asset classes. We’re also hearing increasing interest in sub themes such as biodiversity, water, and energy, which are also key themes for Allspring this year.

A final word

Sustainability factors affect most of the economy. It’s logical that investors today prioritize identifying and managing climate risks in particular. They also realize that, to compete and attract capital, firms must have thoughtful, robust strategies to manage climate and other sustainability trends. Allspring brings highly developed sustainability research and investment capabilities to determine which firms are leading or lagging in their efforts. We look to continually improve these capabilities as climate milestones are reached and as the investing landscape evolves.

1. “Nature Risk Rising: Why the Crisis Engulfing Nature Matters for Business ad the Economy,” World Economic Forum, January 2020.

2. National Geographic, United Nations World Water Development Report, and Nature Journal.

3. “A Climate Finance Framework: Decisive Action to Deliver on the Paris Agreement,” Independent High Level Expert Group on Climate Finance, November 2023.

Related insights

Insight

2023 Stewardship Annual ReportRead about Allspring’s stewardship efforts as we aim to advance the financial, operational, and sustainability performance along with the risk management of investee companies for years to come.

This material is provided for informational purposes only and is for professional/institutional and qualified clients/investors only. Not for retail use outside the U.S. Recipients who do not wish to be treated as professional/institutional or qualified clients/investors should notify their Allspring contact immediately.

THIS CONTENT AND THE INFORMATION WITHIN DO NOT CONSTITUTE AN OFFER OR SOLICITATION IN ANY JURISDICTION WHERE OR TO ANY PERSON TO WHOM IT WOULD BE UNAUTHORIZED OR UNLAWFUL TO DO SO AND SHOULD NOT BE CONSIDERED INVESTMENT ADVICE, AN INVESTMENT RECOMMENDATION, OR INVESTMENT RESEARCH IN ANY JURISDICTION.

INVESTMENT RISKS: All investments contain risk. Your capital may be at risk. The value, price, or income of investments or financial instruments can fall as well as rise and is not guaranteed. You may not get back the amount originally invested. Past performance is not a guarantee or reliable indicator of future results.

Unless otherwise stated, Allspring is the source of all data (which is current or as of the date stated). Content is provided for informational purposes only. Views, opinions, assumptions, or estimates are not necessarily those of Allspring or their affiliates and there is no representation regarding their adequacy, accuracy, or completeness. They should not be relied upon and may be subject to change without notice.