One of the Top Reasons for Retiring Early: Unexpected Job Loss

Many factors must come together to yield good retirement outcomes. One of those critical inputs? The retirement date.

Key takeaways

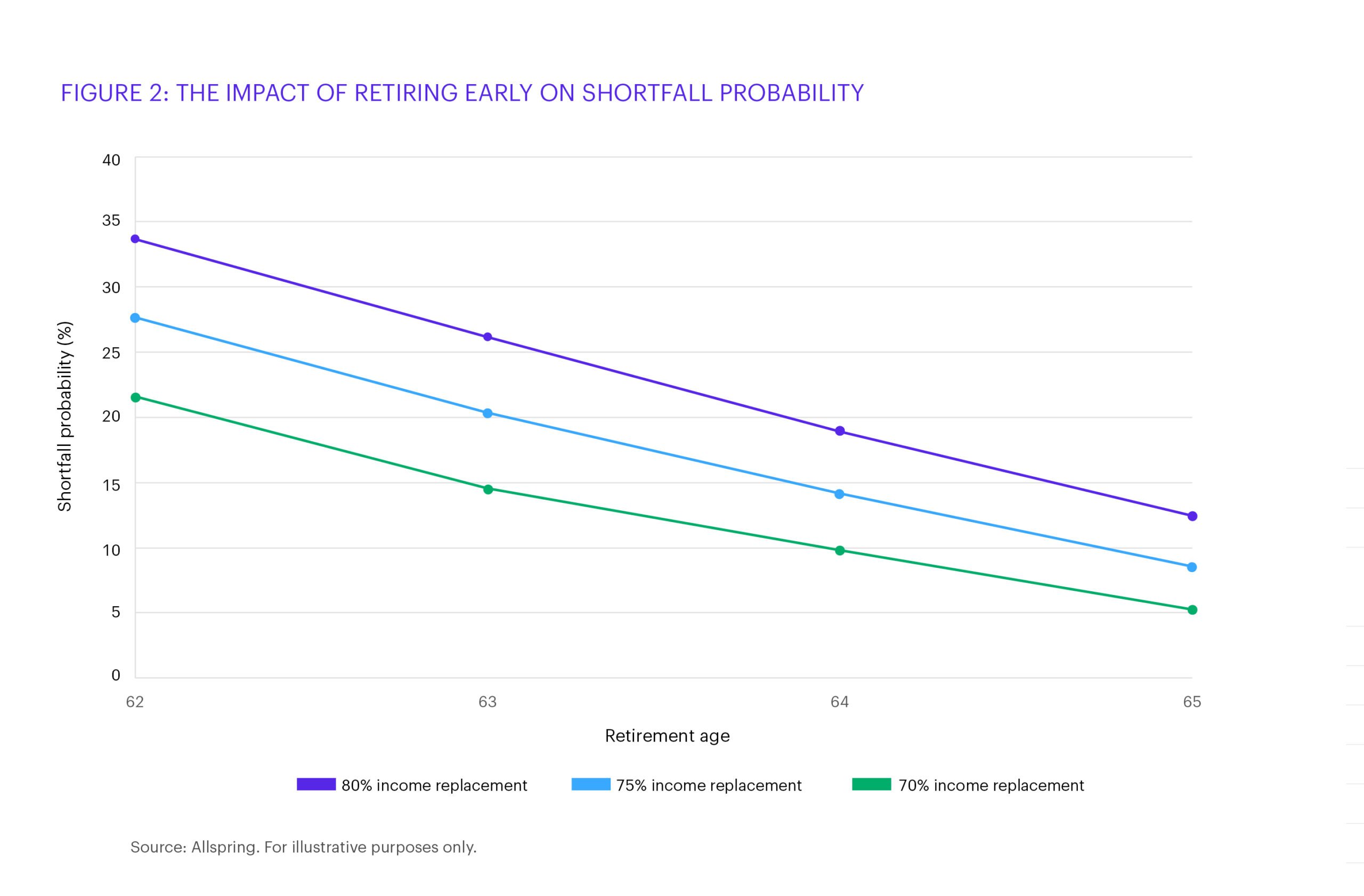

- Our work shows that retiring early raises shortfall risk from 12% to 34%.

- A way to prepare for an earlier-than-expected retirement, from job loss or for other reasons, is to start saving earlier.

- Plan sponsors can investigate the actual retirement age distribution of beneficiaries to determine if sponsor assumptions are still accurate.

Retiring too early means the retirement savings balance might not have grown to the level needed. All else being equal, the earlier the retirement date the longer a retiree will need their retirement balance to last. A smaller balance over a longer time frame means less income and/or more risk.

According to Allspring’s 20th annual retirement study, when an individual retires may not be entirely up to them. In fact, 45% of retiree respondents left the work force earlier than expected, even as the expected retirement age remained constant. For those retirees, the second-most-common reason for early retirement was an unexpected job loss.[1]

Figure 1: Retirees typically retired early due to financial progress or unexpected job loss

| RETIREE (N = 572) | |

|---|---|

| Accelerated financial progress | 28% |

| Unexpected job loss (layoff or firing) | 22% |

| Personal health issues | 21% |

| Health issues of family member(s) | 10% |

| Unexpected financial windfall | 8% |

| Unhappy at work | 7% |

| Offered early retirement/buy-out | 5% |

| Met requirements/able to retire | 5% |

| Other | 15% |

Source: Allspring

This difference between expectation and reality can significantly affect whether there is enough income in retirement. A common way to determine this is to look at the amount of retirement savings needed to replace a percentage of preretirement income. The gap between savings accumulated and savings required is known as the shortfall risk. Assuming a standard retirement age of 65 and a goal of meeting 75% of preretirement income, we estimate the average shortfall risk is 12%—in other words, 12% of 65-year-old retirees have less than 75% of their preretirement income, on average. That 12% shortfall risk increases significantly for earlier retirement ages. Our work shows that retiring early increases the probability of a shortfall from 12% to 34%.

Save early and save often

One way to better prepare for an earlier-than-planned retirement is to start saving earlier. Retirees who responded to our survey echoed this advice. Asked about retirement financial decisions they regretted, many cited not saving more or not saving earlier. On the flip side of this coin, many retirees said the best thing they did for their finances preretirement was saving.[2]

Figure 3: Regrets about financial decisions before retirement

| RETIREE (N = 901) | |

|---|---|

| Saving more | 19% |

| Saving earlier/saving more early | 18% |

| Better investment choices | 15% |

| Contributing to/maximizing 401(k) | 6% |

Source: Allspring

Figure 4: The best thing retirees did for their finances before retirement

| RETIREE (N = 1,228) | |

|---|---|

| Saving | 29% |

| Contributing to/maximizing 401(k) | 11% |

| Saving early | 11% |

| Investing | 11% |

Source: Allspring

Plan sponsors and advisors can help

Without the ability to go back in time and start saving earlier, what can retirement plan participants do and how can plan sponsors and advisors help?

While the number of defined benefit plans has declined meaningfully over the past couple of decades, the impact an employer has on the expected and actual retirement has not waned. A working paper published by the National Bureau of Economic Research in May 2020 found that while individuals responded to shifts upward in their full retirement age (FRA) as pertains to the start of Social Security benefits, the same was not true for the date at which they stopped working and continued to stay anchored to the old FRA. The paper also found that employer norms can play an important role in determining when employees exit the work force.[3] This suggests a gap between when a participant retires and when they begin to collect Social Security. Findings from Allspring’s latest retirement study also illustrate a gap—33% of near-retiree respondents (who were still working) were already drawing Social Security benefits.[4]

What can stakeholders do? We suggest plan sponsors and advisors investigate the retirement age distribution of each plan to better understand how they stack up against expectations. Have many employees expected to retire at 65 but exited in the years prior? Or did they remain employed until 66 or 67? How has the retirement age changed over the past several years? Have different participant cohorts exited at consistent but different ages? Answers to these and other questions could lead plan sponsors to reevaluate assumptions in their retirement calculators, with the goal of making the default age more realistic.

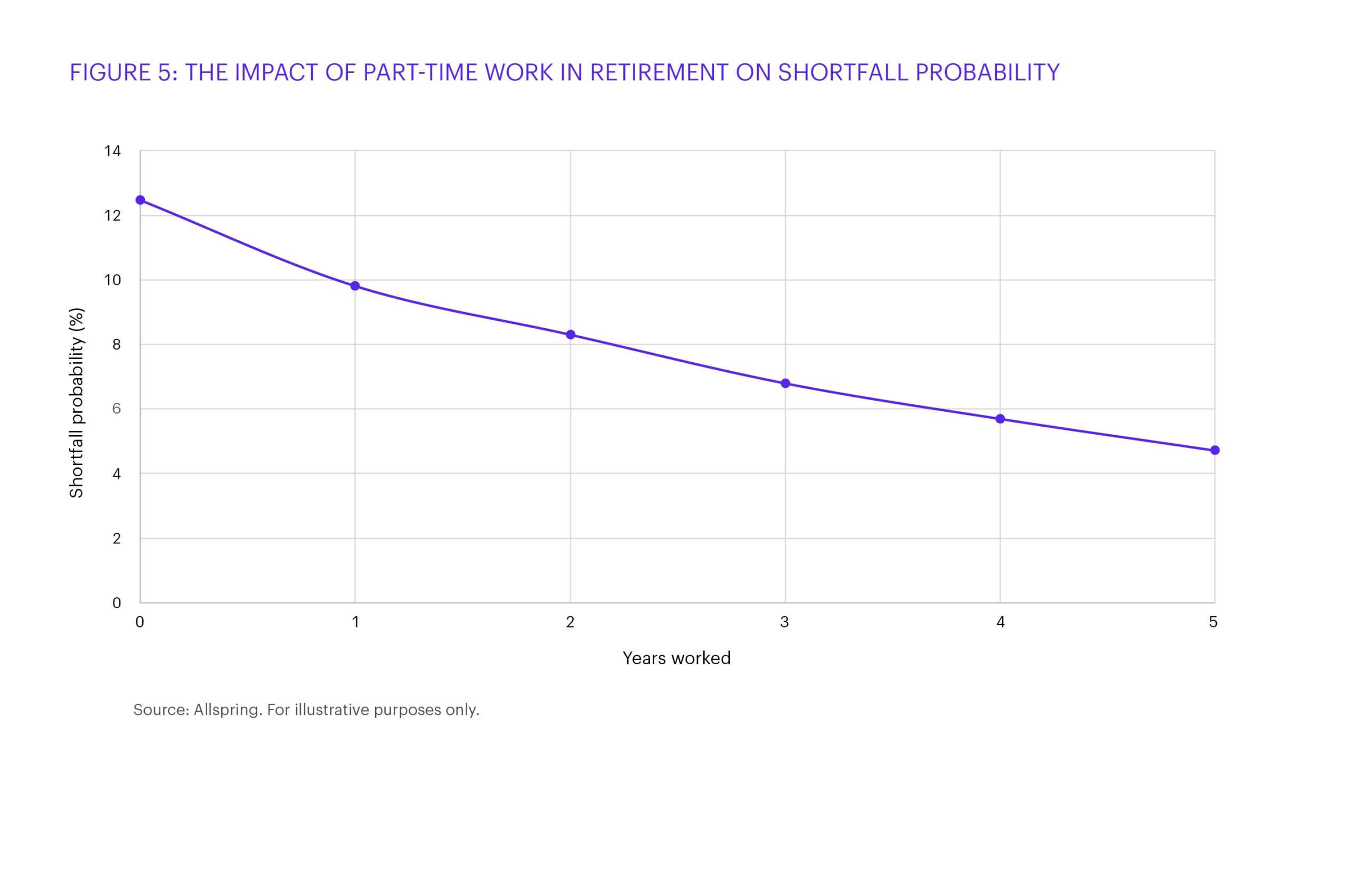

Alternatively, employers could consider adopting work force management programs and/or providing near-retirees with communication materials that highlight the benefits of part-time employment ahead of a full exit. Our work in this area shows these kinds of efforts can significantly reduce shortfall risk.

What individuals can do

We believe individuals should use retirement income calculators in the years leading up to retirement to see how changing their expected retirement age might affect their retirement. These calculators can also show how part-time work early in retirement can help ease the financial burden of retirement. Part-time work also has the potential for maintaining health care benefits prior to Medicare and offers a way to stay engaged with the community. Part-time work may be useful for employees who aren’t fully prepared for retirement and it can help mitigate the biggest downside of retirement identified in our survey—boredom.[5]

Retirement age: More than just a number

Planning for a successful retirement is a key part of financial well-being. Allspring conducts research into retirement readiness to help plan sponsors and advisors work with individuals to foster better outcomes. After all, we know that retirement age is more than just a number and that many factors come into play—from the time that employees become plan participants to when retirees face important decisions about their retirement income.

[1]. Source: Allspring Investor Retirement Study 2022 Q2 (“You previously indicated you were years old when you retired. How did this align with your expectations of when you would retire when you were younger? Did you retire younger than you thought you would be, about the same age, or older than your expectations?”) and Q3 (“What were the primary reasons you retired younger than you expected?”)

[2]. Source: Allspring Investor Retirement Study 2022 Q35 (“Again, looking back on your financial decisions before retirement, any regrets? What’s the one thing you wish you would have done, done earlier, or done differently?”) and Q34 (“Looking back on your financial decisions before retirement, what’s the one thing that you are happiest about doing financially?”)

[3]. Source: Manasi Deshpande, Itzik Fadlon, and Colin Gray. “How Sticky is Retirement Behavior in the U.S.? Responses to Changes in the Full Retirement Age,” Working Paper 27190, National Bureau of Economic Research, May 2020.

[4]. Source: Allspring Investor Retirement Study 2022 Q5 (“Have you personally started collecting Social Security?”)

[5]. Source: Allspring Investor Retirement Study 2022 Q33 (“What do you consider to be the worst part about retirement?”)