Weathering the Risk: A Financial Wake-Up Call for Corporates

Climate-related risks are reshaping financial markets, affecting mortgage lenders, credit ratings, and property investment standards globally.

Authors

-

Kofi Mbuk, Ph.D.

5/19/2025

2 min read

Topic

Sustainable Investing

Key takeaways

- The escalating frequency of wildfires and floods has caused over $2 trillion in financial losses since 2010, with projected losses set to rise by $1.4 trillion by 2030.

- Insurance premiums are surging in high-risk regions, driving shifts in consumer behaviour, mortgage markets, and corporate credit ratings.

- Tools such as Allspring’s Climate Transition framework can potentially help investors identify and manage climate-related risks while uncovering new opportunities.

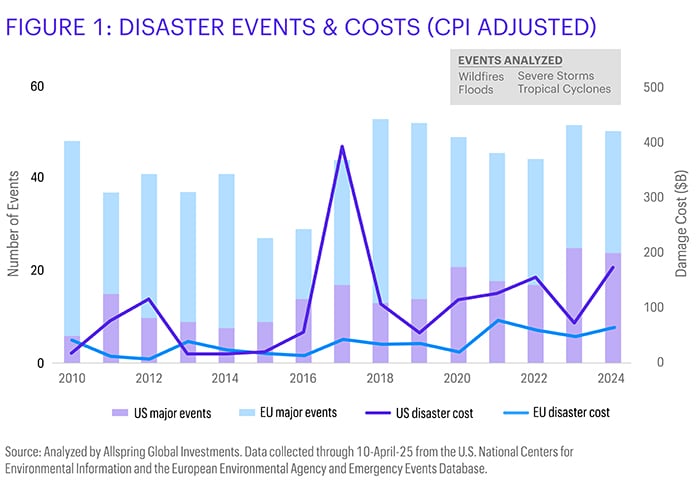

As natural disasters escalate in frequency and severity, the financial toll of wildfires, floods, and extreme weather is mounting rapidly – posing material risks to corporations, insurers, investors, and real estate markets. Since 2010, climate-related disasters have cost over $2 trillion across the U.S. and Europe (see Fig.1), with projected losses expected to reach an additional $1.4 trillion by 2030. This underscores the urgent need for adaptation strategies, smarter risk-pricing, and enhanced risk-management frameworks across sectors.

In both the U.S. and Europe, the effects of rising temperatures have intensified natural hazards. In 2024 – the hottest year on record – communities in the U.S. Pacific states (i.e., California, Oregon, and Washington) experienced widespread devastation from wildfires, while severe flooding and droughts occurred across Europe. These events are not only humanitarian crises but are now driving major shifts in financial markets.

One of the most direct consequences has been the dramatic increase in insurance premiums. In wildfire-prone U.S. Pacific states, 2024 saw homeowner insurance premiums jump 55% above the U.S. average. In hurricane-exposed U.S. South Atlantic states (i.e., Florida, Georgia, Maryland), premiums soared 78% higher than the U.S. average. As insurers reassess their exposure, many have halted issuing new homeowner policies or have pulled out entirely from affected regions – most notably State Farm, Allstate, and Farmers insurance. This has left millions of homeowners with little or no affordable coverage, particularly in markets like Los Angeles and Florida.

The ripple effects of this insurance retreat are becoming increasingly visible. In 2025, Los Angeles County filed a lawsuit for wildfire damages against the utility Southern California Edison, marking a growing trend of litigation aimed at holding corporations accountable for climate-related impacts. Meanwhile, investor concern is growing around real estate and utility companies that have significant exposure to disaster-prone areas. Credit downgrades are increasing, especially where property values have fallen, and insurers have exited.

These market dynamics are also shifting consumer behaviour. Faced with rising premiums or no coverage options at all, many homeowners in high-risk zones are either taking on underinsured risk or dropping their coverage entirely. As a result, mortgage lenders are feeling the impact: since 2021, mortgage delinquencies in high-risk U.S. regions rose by over 90% compared to the national average, eroding the foundations of a relatively stable asset class.

In Europe, flooding and drought are placing comparable strain on economies. Western Europe experienced over $250 billion flood damage between 2013 and 2023, with cities like Paris, Amsterdam, and Venice particularly vulnerable. As insurance claims rise, pressure is mounting on public insurers and government finances. Regulatory initiatives, such as the EU Taxonomy, are starting to require climate resilience in real estate investment standards.

In parallel, the U.S. mortgage and bond markets are being reshaped by these climate-linked risks. Institutions like Freddie Mac and Fannie Mae are increasingly cautious, with reduced appetite for high-risk mortgages. Meanwhile, corporate bonds linked to utilities and real estate firms are facing higher borrowing costs and credit downgrades.

At Allspring, our proprietary framework, the Climate Transition (CT) tool, was built to identify and manage climate-related risks, including the material climate-related physical risks that issuers face. This framework is embedded into certain investment strategies of ours, such as the Climate Transition Investment Grade Credit Strategy, as it allows us to capture both the risks and opportunities arising from the transition to a lower-carbon economy.

This material is provided for informational purposes only and is intended for retail public distribution in the United States. Use outside the United States is for professional/qualified investors only.

ALL-05122025-10svxb09

Related insights

The 30th United Nations Conference of the Parties (COP30) is likely to deliver incremental rather than transformative progress, as most countries remain misaligned with the Paris Agreement and net-zero pathways.