AI at a Crossroads: Concentration, Capex, and What Comes Next

Artificial intelligence (AI) is reshaping markets, with the Magnificent 7 dominating but adding concentration risk. Beyond the leaders, investors can focus on enablers, adopters, and active management to help navigate risk while maintaining exposure.

Key takeaways

- Since 2022, investors have seen both sides of concentration risk. So far in 2026, breadth has improved, but individual stock volatility is higher and dispersion has widened.

- Investors should know how much of their equity risk is coming from the Magnificent 7 and how much exposure they want to AI builders, adopters, and enablers.

- Stock selection matters. In an environment of higher single-stock volatility, active management has the potential to earn its keep, helping with execution and risk control.

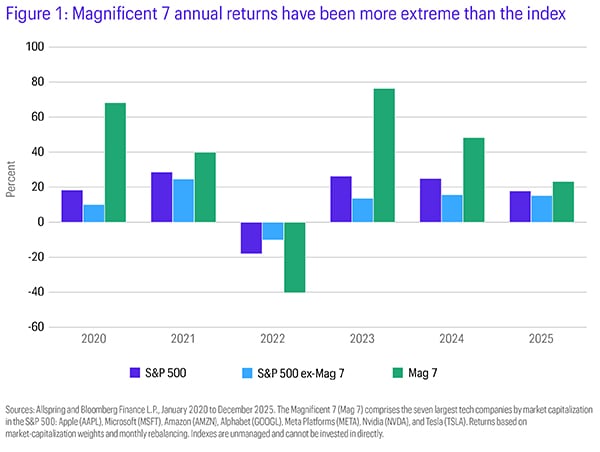

When ChatGPT launched in November 2022, the Magnificent 7 made up roughly 22% of the S&P 500 Index. Just over three years later, they’ve risen to about 32% of the index, as the artificial intelligence (AI) theme has dominated headlines and helped concentrate more of the index into a small group of mega‑cap winners.

As we move through 2026, the picture is more complicated. AI remains the dominant theme, but leadership is wobbling, market breadth is improving, and investors are asking a sharper question: How do I participate in AI without overly relying on a handful of stocks? Our goal is not to call a turning point but to help investors keep exposure to AI’s long‑run potential while managing concentration risk and a maturing capital expenditure cycle.

Years of whiplash

Since 2022, investors have seen both sides of concentration risk (Figure 1). First came the sell-off: Several marquee names dropped 50–70% in a single year. Then came the snapback: In 2023–2024, many of those same companies more than doubled, and some did far better. During that rebound, owning the leaders was essential—avoiding them meant lagging the benchmark.

This year, returns of the Mag 7 basket are softer, while the equal‑weight S&P 500 is positive. Breadth has improved; more individual stocks are outperforming the index. That’s healthy, but it also hides an important reality: Individual stock volatility is elevated, and dispersion between winners and losers has widened. In this environment, we believe selection matters. Crucially, a period of broadening leadership can coexist with a durable multiyear AI trend.

The AI buildout: From spend more to prove more

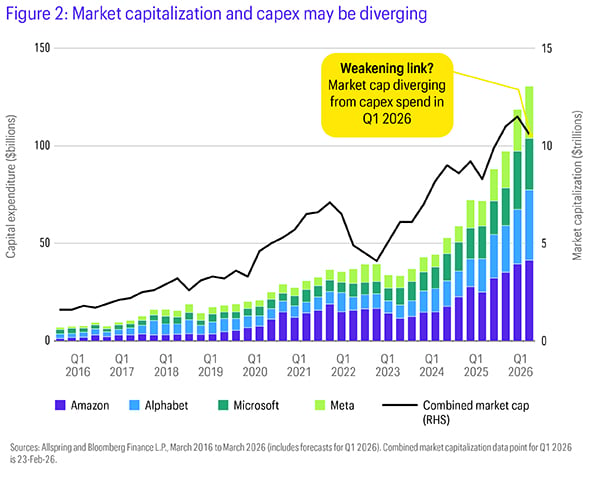

What’s driving this investing crosscurrent is the AI infrastructure race. The largest U.S. tech firms and a growing list of enablers are building data centers, buying advanced chips, expanding networks, and securing power at a breathtaking pace. For much of 2023–2025, markets treated larger AI capex as a leadership signal and often rewarded it.

In 2026, that link seems to have weakened (Figure 2). Investors are starting to separate capex from outcomes. Companies that translate spend into adoption, earn recurring revenue, and demonstrate durable margins continue to be rewarded. Those that scale investment without a clear monetization path are seeing more muted reactions—even if they remain central to the AI story. The focus has shifted from “How much are you spending?” to “What is the return on that spend?” We also believe ambition still matters, but execution efficiency, unit economics, and capital discipline are back in charge. One practical implication: Formerly “asset‑light” platforms are increasingly capital intensive. Sustaining margins now depends on very large, recurring revenue streams to cover depreciation, energy, and refresh cycles.

Bubble or transformation: Two plausible stories

The bear view: Fragility beneath the surface

- Financing risk: Parts of the AI boom rely on complex funding structures that may not age well if conditions tighten.

- Asset life risk: Core hardware, especially graphics processing units (GPUs), can become obsolete quickly, raising the odds of stranded capital if demand or technology turns.

- Ecosystem concentration: A relatively small group of firms drives a large share of AI spending and usage, creating dependencies.

- Expectations risk: For some leaders, valuations still imply near‑perfect execution over multiple years.

- Business‑model shift: Moving from an asset‑light to a high‑capex profile raises the bar for maintaining margins and returns through cycles.

The bull view: Early days in the structural shift

- Real adoption: AI is moving from pilots to embedded workflows—coding, customer service, analytics, design, marketing, and more.

- Productivity gains: Companies report tangible time savings and faster iteration; early benefits are already visible.

- Financial resilience: The largest AI investors have fortress balance sheets and cash flows to sustain multiyear build-outs.

- Broader ecosystem: Opportunity extends beyond the headliners to chips and tools, equipment and networking, data center operators, software platforms, and cybersecurity.

Both stories can be true at once. AI is transformative, and markets are becoming more selective about who will monetize it, when, and at what return on capital.

Practical guidance for portfolios

Investors don’t need to choose between going all in on mega caps or avoiding them. We believe the smarter move is to participate and be intentional about where portfolio risk is likely to arise. Markets are shifting from “spend more” to “prove returns.” That’s a constructive setup for long‑term AI exposure that balances leadership with breadth.

Two key questions remain, with three important insights to consider:

- How much of your equity risk is coming from seven stocks?

- Do you want AI exposure mainly through builders (capex) or adopters (productivity/earnings), and where do enablers fit?

We believe investors should consider three approaches: maintaining but limiting exposure to mega caps, broadening exposure to other AI-related companies, and incorporating active management.

1) Keep the AI leaders but cap concentration.

Mega caps still sit at the center of the AI ecosystem. Their scale, data advantages, and cash flow resilience make them important long‑term beneficiaries. Consider keeping them as a core allocation, rightsized so they don’t dominate total portfolio risk.

2) Broaden exposure beyond the U.S. mega caps (where the next leg of breadth can come from).

Beyond the headliners, there are companies enabling and applying AI across the stack:

- Semiconductors and equipment—top-line “pick and shovel” firms powering AI compute

- Data center and power infrastructure—where capacity, efficiency, and energy access are becoming bottlenecks

- Enterprise software and cybersecurity—turning AI into recurring revenue and workflow stickiness

And don’t overlook diversification. Small- and mid-cap stocks and non-U.S. equities may offer exposure to innovation while reducing dependence on one U.S. mega-cap cycle. Investors should know how their portfolio is positioned:

- Concentration: What percent of equity exposure sits in the top 10 holdings and the Magnificent 7?

- Factors: How much recent return came from mega‑cap growth or momentum?

- AI map: Are you tilted more toward builders, enablers, or adopters?

3) Use active management to harness dispersion.

In an environment of higher single-stock volatility and wider spreads between winners and laggards, active management has the potential to earn its keep. We believe the next phase is likely to reward execution, cash flow visibility, and capital discipline and punish undifferentiated spend.

Bottom line

AI has changed markets quickly, but the next phase will be more selective. Not every firm that spends will win, and not every “AI beneficiary” will deliver. Concentration remains high, breadth is improving, and the market is separating capex from outcomes.

For investors, the objective may be simple: Stay in the AI game, broaden the bench, and rebalance the risks. In our view, the answer may be to keep core exposure to the leaders, add the right enablers and adopters across the value chain, and use active management to focus on execution and risk control. In a market with elevated dispersion, how you own AI matters as much as whether you own it.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

Diversification does not ensure or guarantee better performance and cannot eliminate the risk of investment losses.

The S&P 500 Index consists of 500 stocks chosen for market size, liquidity, and industry group representation. It is a market-value-weighted index with each stock’s weight in the index proportionate to its market value. You cannot invest directly in an index.

This material is provided for informational purposes only and is intended for retail public distribution in the United States. Use outside the United States is for professional/qualified investors only.

ALL-03042026-cvfcjjx4

Related insights

John Campbell reviews Q1 volatility, emphasizing risk management and strategic focus amid uncertainty.

Alison Shimada highlights emerging markets' resilience, global importance, and investment opportunities amid geopolitical challenges.

As passive investing dominates market flows, John Campbell, head of Systematic Core Equity at Allspring Global Investments, examines the risks of peak passive concentration and the case for broader diversification.

Emerging markets (EM) have undergone a structural shift, with stronger external balances, rising credit quality, and broadening earnings growth reshaping their risk profile and investment appeal in 2026.

Listen to John Campbell from our Systematic Core Equity team discuss how multiple perspectives reveal the full picture of risk.

John Campbell reviews 2025's market performance, highlights elevated factor risks, and emphasizes a multidimensional approach to risk management and diversification for 2026.

Bryant VanCronkhite highlights the evolving AI landscape, a shift in small-cap market dynamics, and the potential for a massive multi-industry upgrade cycle driving economic and market growth in 2026.

Alison Shimada and Derrick Irwin discuss why now presents a pivotal time for investors looking at the asset class. Discover the shifting global dynamics and themes shaping the future of emerging markets (EMs) from two different perspectives.

The global landscape is shifting, and structural tailwinds are lifting emerging market (EM) equities. Investors capitalizing on these trends could benefit from transformative growth opportunities for years to come.

Video

The Dividend DivideAllspring experts explore the evolving role of dividends, debating their value as a source of stability, a tool for discipline, and their impact on flexibility in today's market.

Hyperscalers are investing in artificial intelligence (AI) and infrastructure to drive innovation while navigating challenges—balancing short-term demands with long-term growth opportunities.

Allspring equity portfolio managers Bryant VanCronkhite, Alison Shimada, and Mike Smith sit down to explore current market conditions, economic uncertainties, and potential investment strategies for 2025. They break down the unique challenges and opportunities in current equity markets and the importance of active management and resilience during times of volatility.