Beyond the Mag 7: Investing Across the AI Ecosystem

AI investing is moving beyond the Magnificent 7. As adoption spreads, opportunities are emerging across the broader ecosystem—from infrastructure to real-world applications—making a more diversified, multi-layered approach increasingly important.

7/1/2026

4 min read

Topic

Equities

Key takeaways

- Artificial intelligence (AI) opportunity is broadening: Value creation is expanding beyond mega-cap infrastructure into implementation and real-world applications.

- Diversification is increasingly important: Overconcentration in the Magnificent (Mag) 71 may limit exposure to the full AI opportunity set.

- Barbell approach may be effective: Maintaining core exposure to incumbents while adding “edge” beneficiaries may help capture multiple phases of growth.

- Earnings growth is evolving: As adoption widens, earnings inflection could emerge across a broader group of companies and sectors.

- Sector opportunities are expanding: Industrials and financials are well positioned to benefit from both productivity gains and new revenue opportunities driven by AI.

Capturing the evolution of AI

As AI capital expenditures expand across the technology value chain, we believe a holistic investment approach is increasingly important. While mega-cap companies, particularly the Mag 7, are likely to remain central to the AI build-out, investors may benefit from broadening their exposure beyond these dominant players.

The AI ecosystem can be thought of as consisting of five distinct layers. Diversified exposure across these layers may provide broader participation in the evolving opportunity set.

Exhibit 1: Multiple layers of AI

FIVE-LAYER ARCHITECTURE OF THE AI STACK

1. Energy and power infrastructure

This foundational layer includes power generation and grid modernization to support AI’s high energy demands. ETN, TT, XYL, SU, and TTE

2. Chips and computing infrastructure

This layer provides semiconductor design, GPUs, and hardware essential for high-performance AI computing. AMD, LRCX, NVDA, ADI, and ASML

3. Cloud data centers

Cloud platforms aggregate compute resources, offering scalable and reliable AI processing worldwide. AMZN, GOOG, MSFT, and SPCX

4. AI models

This core layer encompasses foundational and large language models enabling advanced reasoning and content generation. SPCX, OpenAI, and Anthropic

5. Applications adopters

AI applications deliver value across industries, driving automation, decision support, and productivity gains. Software, JPM, LLY, HLT, SPCX, industrials, and financials

Source: Allspring. The securities listed above should not be considered a recommendation to purchase or sell any particular security.

The case for a broader allocation

The AI infrastructure build-out has been rapid and capital-intensive. As this phase matures, we expect spending to increasingly shift toward implementation and application across the broader value chain. This evolution could create opportunities in areas such as software, industrial technology, data procurement, and real-world AI use cases.

At the end of 2025, a valuation gap existed between the Mag 7 and the remainder of the S&P 500, with the Mag 7 trading at approximately 22x earnings versus roughly 17x for the rest of the index.2 As AI adoption broadens and earnings growth inflects upward across a wider set of companies, this disparity could narrow, potentially driving a rotation toward more diversified exposure. While early signs of this trend have emerged, we believe its full extent still lies ahead.

Our investment approach

Against this backdrop, we are employing a barbell approach, balancing exposure to established leaders with emerging AI beneficiaries.

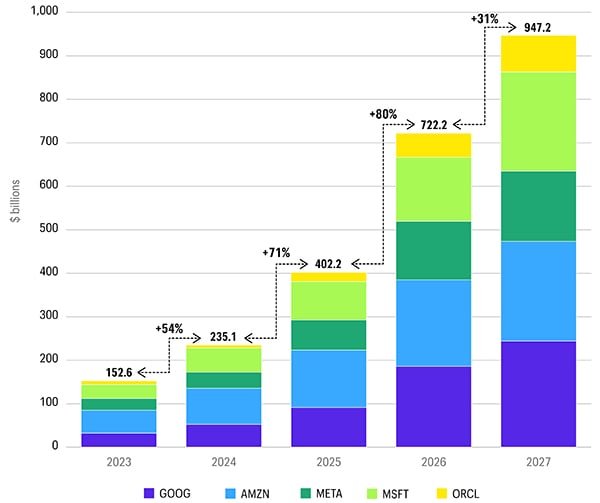

On one end of the barbell, we maintain exposure to the Mag 7 with reduced position sizes. These companies remain key beneficiaries of ongoing AI-related capital expenditures. Spending among the largest players is projected to reach approximately $722 billion in 2026 and $947 billion in 2027, with some estimates exceeding $1 trillion over that period. We believe this underscores the durability of the current investment cycle, though outcomes may vary.2

Exhibit 2: Capital expenditures

Source: Bloomberg Finance L.P. Consensus estimates as of 17-Jun-26. The securities listed above should not be considered a recommendation to purchase or sell any particular security.

At the other end, we are increasingly focused on identifying opportunities at the “edges” of the AI ecosystem—companies with less direct or underrecognized exposure to AI where earnings growth may begin to accelerate. As productivity gains materialize and monetization improves, these companies could see valuations expand, potentially creating attractive stock-specific return opportunities.

Recent developments reinforce this view. For example, results from companies such as ASML Holding N.V. (ASML) and Taiwan Semiconductor Manufacturing Co. Ltd. (TSM) suggest that demand for compute remains strong. Looking ahead, the shift from generative AI to agentic AI may result in higher levels of token consumption (that is, AI processing activity), which could help drive the next phase of AI applications.

Beneficiaries of a broadening AI ecosystem

As the AI theme evolves, certain sectors appear particularly well positioned to benefit.

Industrials offer a compelling mix of secular and cyclical exposure. AI adoption across capital goods and diversified industrials is expanding, with potential applications in product design, engineering, factory automation, labor productivity, predictive maintenance, and pricing optimization. We believe rising investor interest reflects a broader effort to identify AI-linked opportunities with tangible, near-term earnings impact.

Financials, particularly banks, may benefit in multiple ways. While productivity improvements are an important component, the opportunity extends beyond cost efficiencies. Potential applications include credit underwriting, pricing optimization, fraud detection, and risk management. These use cases may span not only consumer banking but also corporate and investment banking as well as asset and wealth management. Additionally, enhanced data capabilities could support improved cross-selling and client engagement, contributing to revenue growth over time.

Positioning for the next phase of AI

The AI investment opportunity is evolving beyond its initial infrastructure-driven phase and broadening across the economy. As capital moves downstream toward implementation and real-world application, relying solely on mega-cap exposure may limit participation in the next phase of value creation.

A diversified, layered approach, combining exposure to established compounders with emerging companies positioned to benefit from the expansion of AI adoption, can offer a more balanced way to capture this evolution. While outcomes are not guaranteed, investors positioned across multiple segments of the AI value chain may be better equipped to navigate and participate in the next wave of technological innovation.

Related insights

As global investors look to broaden their opportunity set, emerging markets small caps may offer a differentiated path to growth, diversification, and active management alpha.

A risk-on rally fueled by AI and earnings strength set the tone, but elevated expectations and macro uncertainty may shape a more volatile path ahead. Allspring’s Head of Systematic Core Equity, John Campbell, recaps second-quarter market performance and highlights the importance of diversification and risk management.

Despite heightened geopolitical volatility, emerging markets remain undervalued and under-owned, with long term structural tailwinds creating compelling opportunities for active investors.

John Campbell reviews Q1 volatility, emphasizing risk management and strategic focus amid uncertainty.

Alison Shimada highlights emerging markets' resilience, global importance, and investment opportunities amid geopolitical challenges.

As passive investing dominates market flows, John Campbell, head of Systematic Core Equity at Allspring Global Investments, examines the risks of peak passive concentration and the case for broader diversification.

Emerging markets (EM) have undergone a structural shift, with stronger external balances, rising credit quality, and broadening earnings growth reshaping their risk profile and investment appeal in 2026.

Listen to John Campbell from our Systematic Core Equity team discuss how multiple perspectives reveal the full picture of risk.

John Campbell reviews 2025's market performance, highlights elevated factor risks, and emphasizes a multidimensional approach to risk management and diversification for 2026.

Bryant VanCronkhite highlights the evolving AI landscape, a shift in small-cap market dynamics, and the potential for a massive multi-industry upgrade cycle driving economic and market growth in 2026.

Alison Shimada and Derrick Irwin discuss why now presents a pivotal time for investors looking at the asset class. Discover the shifting global dynamics and themes shaping the future of emerging markets (EMs) from two different perspectives.

The global landscape is shifting, and structural tailwinds are lifting emerging market (EM) equities. Investors capitalizing on these trends could benefit from transformative growth opportunities for years to come.

1. The “Magnificent 7” comprises the seven largest tech companies by market capitalization in the S&P 500 as of 3/31/2026: Apple (AAPL), Microsoft (MSFT), Amazon (AMZN), Alphabet (GOOGL), Meta Platforms (META), Nvidia (NVDA), and Tesla (TSLA).

2. Source: Bloomberg Finance L.P.

Standard & Poor’s 500 Index (S&P 500 Index)

The S&P 500 Index consists of 500 stocks chosen for market size, liquidity, and industry group representation. It is a market-value-weighted index with each stock’s weight in the index proportionate to its market value. You cannot invest directly in an index.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

All investing involves risks, including the possible loss of principal. There can be no assurance that any investment strategy will be successful. Investments fluctuate with changes in market and economic conditions and in different environments due to numerous factors, some of which may be unpredictable. Each asset class has its own risk and return characteristics.

This material is provided for informational purposes only and is intended for retail distribution in the United States.

Diversification does not ensure or guarantee better performance and cannot eliminate the risk of investment losses.

ALL-07072026-dhiapmoz