Income Generator: Navigating the Credit Supercycle

George Bory and Jamie Newton discuss global credit markets amid rising dispersion, structural shifts, and AI-driven investing, urging fixed income investors to consider active strategies with global diversification and sector selectivity.

Key takeaways

- Shift in credit dynamics: The credit market appears to be transitioning from broad beta-driven returns to a phase marked by dispersion, structural changes, and idiosyncratic risks.

- AI's dual impact: AI is reshaping credit markets both technically (through funding needs) and fundamentally (disruption and disintermediation).

- Active strategies may be vital: In a maturing cycle, global diversification, sector selectivity, and issuer-level research are critical for navigating risks and capturing opportunities.

A supportive but maturing macro backdrop

The macroeconomic foundation for credit remains generally constructive. Global growth has proven resilient through the post‑pandemic normalization, with consensus forecasts pointing to trend‑like expansion. However, renewed conflict in the Middle East has disrupted expectations for a smooth disinflation path and reintroduced downside risks to near‑term growth. While the mix of growth may evolve, the overall level continues to support corporate revenues and margins, reinforced by broadly healthy balance sheets across both investment grade and high yield.

With operating margins near 19%, U.S. corporate profitability remains robust1 and defaults in high yield bonds and leveraged loans remain low by historical standards. Moreover, much outstanding corporate debt was issued at historically low coupons, limiting the near‑term impact of higher rates. That said, the cycle is maturing. Aggregate strength increasingly masks dispersion beneath the surface. The macro tailwind is no longer sufficient on its own to drive returns, and investors must be more deliberate in identifying where compensation for risk remains attractive.

Credit fundamentals: Strength with growing divergence

Corporate balance sheets for many investment-grade and high yield companies entered this cycle in strong shape, as many issuers took advantage of low borrowing costs to extend liabilities over the prior 10 years. Leverage ratios remain broadly manageable, and interest coverage metrics, while trending lower as rates rise, are still supportive of credit quality for most issuers.

However, credit risk has become far more idiosyncratic. Sectoral differences, business‑model resilience, and capital allocation decisions now appear to matter more than broad economic conditions. Some issuers face structural headwinds from technological disruption or rising capital intensity, while others benefit from pricing power, financial flexibility, or secular growth drivers.

For credit investors, this shift underscores the limits of index‑oriented approaches. As dispersion increases, alpha generation depends more heavily on security selection, issuer‑level research, and relative‑value analysis across capital structures.

Technical crowding in: Demand meets record supply

One of the defining features of today’s credit environment is technical crowding in. Investor demand for fixed income has remained exceptionally strong, driven by higher all‑in yields, portfolio rebalancing, and the need for income and diversification. At the same time, corporate issuance has surged and kept technicals rather balanced.

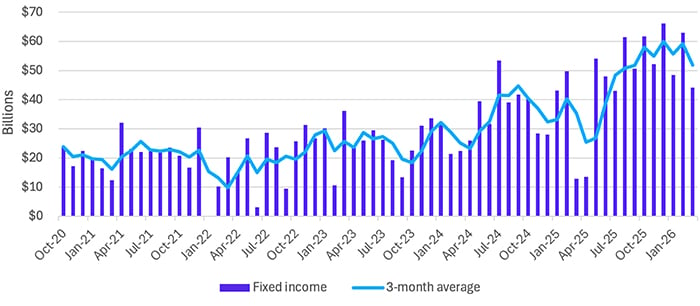

Figure 1: Demand for fixed income

Net fixed income ETF flows. Sources: Allspring and Bloomberg Finance L.P., as of 31-Mar-26

Investment‑grade corporate supply is projected to reach record levels, reflecting refinancing activity; merger and acquisition (M&A) activity; and, increasingly, capital expenditures tied to digital infrastructure and AI. Despite this surge in supply, spreads have remained tight—even after recent bouts of widening—supported by attractive valuations, persistent inflows, and limited alternatives for yield‑seeking investors.

This environment has created a crowded trade, with large segments of the credit market heavily owned and therefore more vulnerable to shifts in investor sentiment or liquidity conditions. While spreads widened due to geopolitical risks and inflation pressures recently, they remain somewhat tight relative to historical norms and no longer provide uniform compensation for risk, particularly in areas where fundamentals are deteriorating or leverage is poised to rise.

AI as a source of fundamental crowding out

AI represents a powerful structural force reshaping credit markets. Hyper-scalers and related technology ecosystems are undertaking an unprecedented investment cycle, driving massive spending on data centers, energy infrastructure, and computing capacity. From a credit perspective, this capital intensity raises questions around returns on invested capital, leverage, and long‑term cash flow durability. While many issuers are well positioned to absorb these investments and generate sustainable earnings growth, others may face pressure if expected benefits fail to materialize.

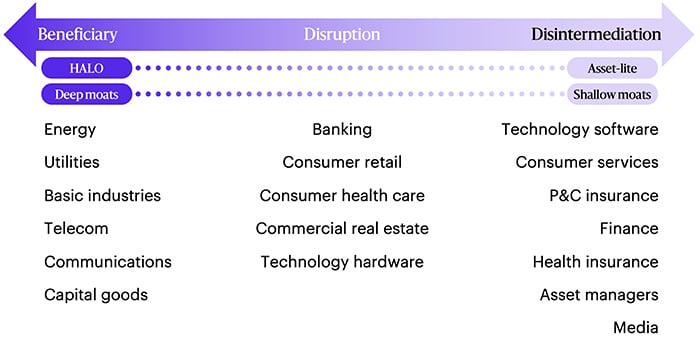

AI is poised to drive efficiencies and potentially disrupt or disintermediate businesses, which raise the significance of “HALOs” (hard assets, low obsolescence) and “moats.” Companies with hard assets and low obsolescence (HALO) are well positioned to incorporate the benefits of AI with limited disruption to their business model. Conversely, companies heavily dependent on digital assets and/or intellectual capital may be at risk of more meaningful disintermediation, unless the industry is protected by a “moat” such as regulations, proprietary assets, or emotional connections.

Figure 2: AI fundamental transformation

Source: Allspring Fixed Income Research, as of 31-Mar-26.

The dispersion between AI winners and losers is likely to widen as the AI revolution broadens, reinforcing the case for selective exposure rather than broad market allocations.

Identifying pockets of value in a credit supercycle

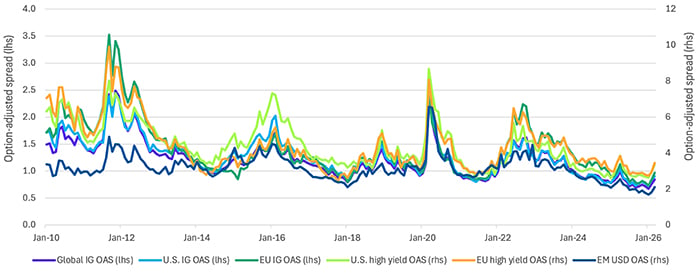

Figure 3: Credit spreads remain tight

Source: Bloomberg Finance L.P. Bloomberg Global Bond Indices, as of 31-Mar-26. OAS = option-adjusted spread. IG = investment-grade.

Indices listed: Global IG OAS = Bloomberg Global Agg Credit Total Return Index Value Unhedged USD Index, U.S. IG OAS = Bloomberg

US Corporate Total Return Value Unhedged USD Index, EU IG OAS = Bloomberg Pan-European Aggregate Corporate Total Return Index

Value Unhedged (EUR) Index, U.S. high yield OAS = Bloomberg US Corporate High Yield Total Return Index Value Unhedged USD Index,

EU high yield OAS = Bloomberg Pan-European High Yield Total Return Index Value Unhedged USD Index, EM USD OAS = Bloomberg

Emerging Markets USD Aggregate Bond Index.

Despite tighter-than-average headline spreads, opportunities remain for active investors willing to look beyond the most crowded segments of the market. Several themes stand out:

Global diversification: Non‑U.S. credit markets, particularly in Europe and emerging markets, have shown periods of outperformance relative to the U.S. in both investment-grade and high yield segments. Differences in monetary policy cycles, sector composition, and investor bases can create relative‑value opportunities for global allocators.

Cyclical and capital-intense sectors: Energy, food, and commodity‑linked sectors can offer attractive compensation where balance sheets are disciplined and cash flows are supported by structural demand or constrained supply.

Capital‑structure complexity: Within single issuers, valuation dislocations between senior, subordinated, and hybrid securities can provide opportunities to enhance returns without materially increasing default risk.

Rising dispersion: As spreads continue to trade in a long‑term downward channel, the growing dispersion across sectors, ratings, and issuers increases the potential payoff to security selection.

Key risks to monitor

A constructive credit outlook does not imply the absence of risk. Several factors warrant close attention:

- AI investment risk: The scale and speed of AI‑related capital spending introduce uncertainty around execution, profitability, and leverage trajectories.

- Geopolitical fragmentation: A multipolar world, with heightened tensions across regions, raises the risk of supply chain disruptions, sanctions, and market volatility.

- Private credit growth: After the rapid expansion of private credit—often with less transparency, less liquidity, and higher leverage—concerns are increasing regarding hidden interconnections with public markets.

- Renewed M&A activity: A pickup in mergers and leveraged transactions could pressure credit quality, particularly if financed aggressively.

Rethinking credit allocation

Credit markets remain supported by resilient macro fundamentals and strong technicals, but crowding and dispersion increasingly define outcomes. In a crowded trade, risk and return are no longer evenly distributed. In our opinion, investors who rethink traditional exposures and embrace active, research‑driven strategies will be better positioned to navigate the next phase of the credit cycle and capture durable income and total return.

1. Consensus estimates 2026 S&P 500 operating margins, from Bloomberg Finance L.P., as of 31-Mar-26.

The Bloomberg Global Agg Credit Total Return Index Value Unhedged USD Index is a subset of the Bloomberg Global Aggregate Index. It measures the performance of global investment-grade, fixed-rate corporate and government-related bonds, including developed and emerging markets, and is reported in USD.

The Bloomberg US Corporate Total Return Value Unhedged USD Index measures the performance of investment-grade, fixed-rate, taxable corporate bonds denominated in USD. It includes industrial, utility, and financial issuers, representing the US dollar-denominated investment-grade corporate market.

The Bloomberg Pan-European Aggregate Corporate Total Return Index Value Unhedged (EUR) Index is a subset of the broader Bloomberg Pan-European Aggregate Index, focusing specifically on corporate bonds within that region.

The Bloomberg US Corporate High Yield Total Return Index Value Unhedged USD Index measures the performance of USD-denominated, non-investment grade, fixed-rate, taxable corporate bonds. It covers the "junk bond" market, focusing on corporate debt rated Ba1/BB+/BB+ or below by Moody's, S&P, or Fitch.

The Bloomberg Pan-European High Yield Total Return Index Value Unhedged USD Index measures the performance of non-investment grade, fixed-rate corporate bonds denominated in European currencies (EUR, GBP, DKK, NOK, SEK, CHF). It offers a USD-unhedged view of the Pan-European high-yield market.

The Bloomberg Emerging Markets USD Aggregate Bond Index is a flagship benchmark designed to measure the performance of fixed and floating-rate, U.S. dollar-denominated debt from sovereign, quasi-sovereign, and corporate issuers in emerging market countries. It is a total return index.

Diversification does not ensure or guarantee better performance and cannot eliminate the risk of investment losses.

All investing involves risks, including the possible loss of principal. There can be no assurance that any investment strategy will be successful. Investments fluctuate with changes in market and economic conditions and in different environments due to numerous factors, some of which may be unpredictable. Each asset class has its own risk and return characteristics.

This material is provided for informational purposes only and is intended for retail public distribution in the United States. Use outside the United States is for professional/qualified investors only.

ALL-04092026-fuuk7qu7

Related insights

George Bory, chief investment strategist for Allspring Fixed Income, explains how active bond investing can enhance outcomes by focusing on investor needs, weighing opportunity costs, and capitalizing on market inefficiencies.

Janet Rilling reviews the dynamic market shifts of Q1, strategies for navigating Q2, and her team’s disciplined approach to managing through volatility.

George Bory explains why bond markets in 2026 should favor discipline and flexibility. Positive real yields, global policy divergence, and credit dispersion may create opportunities for income generation and selective positioning.

Janet Rilling and Hannah Rosencrantz give a Q3 fixed income market update—discussing strong bond performance, potential risks in credit compensation, and strategies for building resilient portfolios in Q4.

Nick Venditti, head of Municipal Fixed Income at Allspring Global Investments, talks about how, for the first time in a while, the higher education sector is starting to show signs of distress.