Macro Matters: A Delicate Global Balance

Which macroeconomic trends do we think matter the most? Read this month’s issue of Macro Matters.

Key takeaways

- Growth: We expect robust U.S. growth through the end of the year, with dispersion more likely in the rest of the world.

- Inflation: China continues to exert a disinflationary impulse, while core inflation remains stubbornly above target in the U.S. and U.K.

- Rates: We expect the Federal Reserve (Fed) to hold rates through December, but labor market weakness remains a key risk.

Economic growth: Optimism for now

United States

The U.S. government shutdown has triggered a dearth of data—for policymakers and market participants. Economic indicators still being published (such as the Atlanta Fed GDPNow estimate) project robust U.S. growth through year-end, with the latest GDPNow reading at 3.93% (as of October 31). The labor market has been a persistent source of concern, with unemployment claims and the unemployment rate continuing to pick up. Until we see the return of published data, we live in an environment of greater uncertainty. News of the U.S.-China trade tensions cooling is also likely to mean the can continues to get kicked down the road.

Eurozone

Growth in the eurozone is low but surprised to the upside, with third quarter growth in gross domestic product (year over year) coming in at 0.3%, or 0.2% above expectations. The recovery has been driven by services, which have accelerated in Germany and the eurozone periphery. Manufacturing has been subdued. As we enter the winter, energy may again begin to dominate. Labor markets seem stable across the region for now. In our view, narratives around fiscal spending will come in much slower than current expectations, which could weigh on 2026 growth forecasts.

China

An improvement in manufacturing and services sentiment data has been accompanied by decent growth in industrial profits, suggesting a growth inflection may be on the horizon. Asset markets have been buoyant, but the region faces structural challenges from consumers amid continued pressure on the property market. The manufacturing sector has been pressured by global trade and tariff uncertainties, amid the push to diversify exports as a top priority.

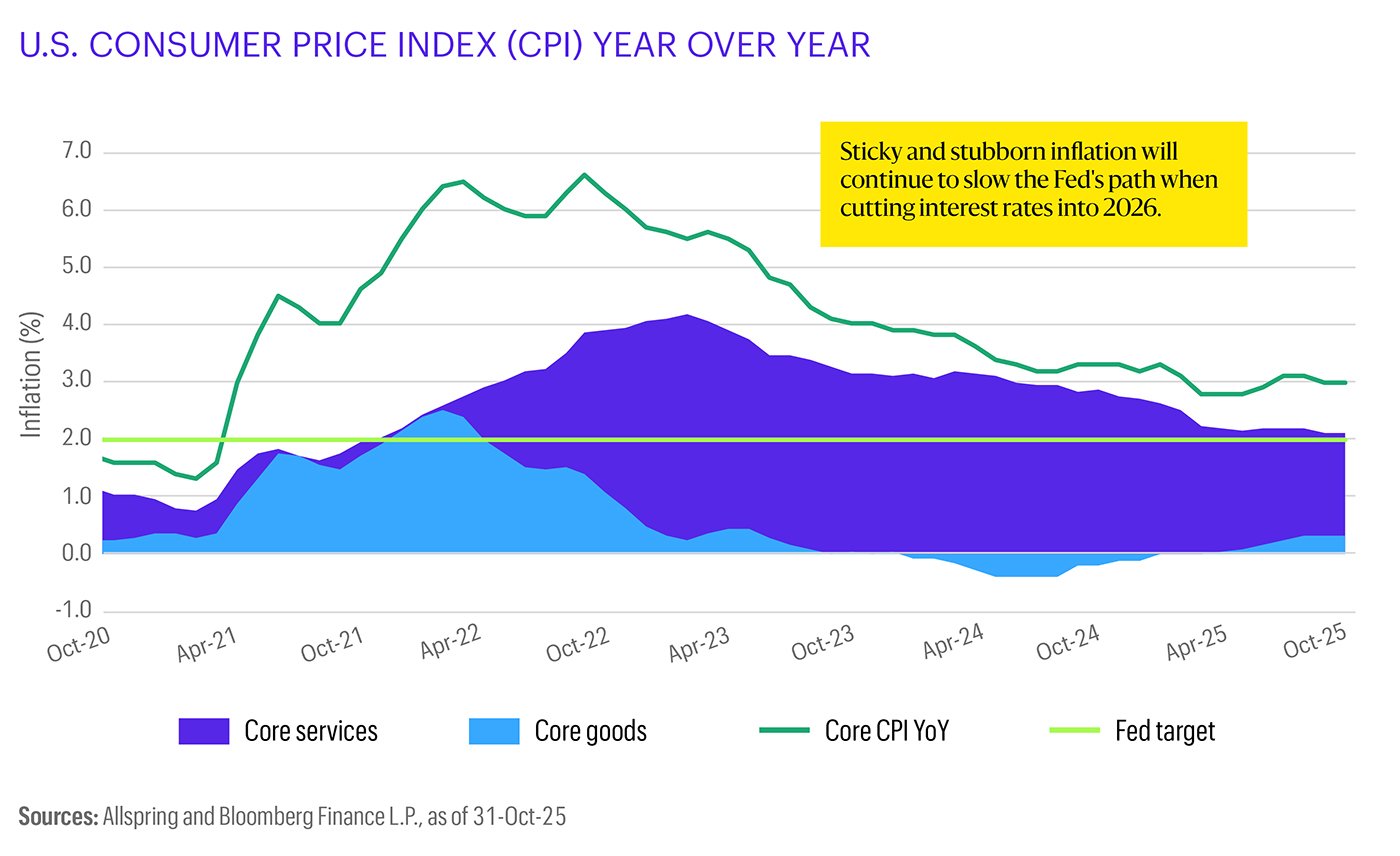

Inflation: Stubborn, but does it matter?

United States

Inflation has remained a challenge in the U.S.—optically, at least. It’s higher than target but, with a strong growth backdrop, does that really matter? Inflation was the one piece of crucial data we did receive in October; it remains to be seen whether the Bureau of Labor Statistics will be recalled again for the November report. Core inflation in the U.S.—the Fed’s preferred measure—was 3.0% in September. Services continue to moderate in price pressure, rising 2.1% in September (year over year), compared with 2.2% in August. Goods price pressures continued to tick up at 0.32% in September (year over year), compared with 0.31% in August. Crucially, we’ve begun to see modest signs of price pressures from tariffs in the data.

Eurozone

Inflation in the eurozone remains close to the European Central Bank’s (ECB) 2.0% target. In the absence of higher growth, the ECB is likely to remain on hold until it sees persistent price pressures building. The fiscal impulse of any area-wide spending will become increasingly important.

China

Deflationary forces have continued to weigh on China, with a 0.3% year-over-year decline in the headline figure for September. Retail sales have continued to moderate, alongside structural weakness in the property market. Further monetary stimulus may be necessary to support the government’s 5% growth target.

Interest rates: Hold, please

United States

As expected, the Federal Open Market Committee (FOMC) announced another 0.25% cut, reducing its key interest rate (the federal funds rate) to 3.75–4.00%. Chair Powell reiterated that the December cut was not a certainty and that inflation had remained more stubborn than they perhaps expected. We believe the FOMC will remain on hold, absent a shock to the labor statistics.

Eurozone

In the eurozone, the ECB has cut its interest rates four times in 2025, down from a high of 4.0% in 2023 to 2.0%. The market has not priced in further cuts, awaiting signs of growth acceleration or labor market deterioration. While external demand has improved, the growth engine is in a tricky spot. Further rate cuts are unlikely to boost real growth but may cushion asset prices.

China

We expect the People's Bank of China to continue easing monetary policy, primarily through the currency and bond channels as opposed to outright changes in the reserve requirements or benchmark rates. China has faced persistent deflation and subdued domestic demand. Tariff negotiations have seemingly struck a truce for the moment and, although a broad agreement is likely, frictions remain.

Investment implications

Fixed income

We believe U.S. sovereign bond markets are fairly priced at the current level—400–410 basis points (bps; 100 bps equal 1.00%) on the 10-year issue—and we don’t expect further rate cuts until early 2026. The balance between growth and inflation seems robust, absent any shocks to the labor market. We believe U.S. bonds will remain range-bound through year-end and still have a steepening bias. Outside the U.S., we like emerging market debt with an attractive carry and currency profile, particularly in local currency. We expect fixed income volatility to ramp up into year-end. We see corporate debt as an attractive source of carry—particularly high yield—but new positions are unlikely here through year-end.

Equities

We've maintained a positive outlook on equities generally and continue to maintain an overweight position on emerging markets. Seeing value in more affordable sectors of the U.S. market, we prefer a barbell approach of high-quality value names plus growth exposure. Earnings momentum has remained positive. We anticipate fourth quarter expectations will ramp up, while we see risks beginning to creep higher. Without further data on the state of the economy, we expect a melt-up in equity markets more generally, albeit with higher volatility into year-end.

Multi-asset portfolios

From a multi-asset perspective, we are constructive on global equities but look to moderate our portfolio overweights, despite attractive valuations. This relates to a shift in our view of a stronger U.S. dollar, as we expect a normalization in currency correlations after a break in the first quarter. Within the U.S., we favor sectors with positive earnings momentum, such as information technology and consumer discretionary, but add to our barbell with other sectors such as utilities. We continue to favor medium-term-maturity bonds over cash. Tariff noise may introduce short-term volatility, which may be an opportunity.

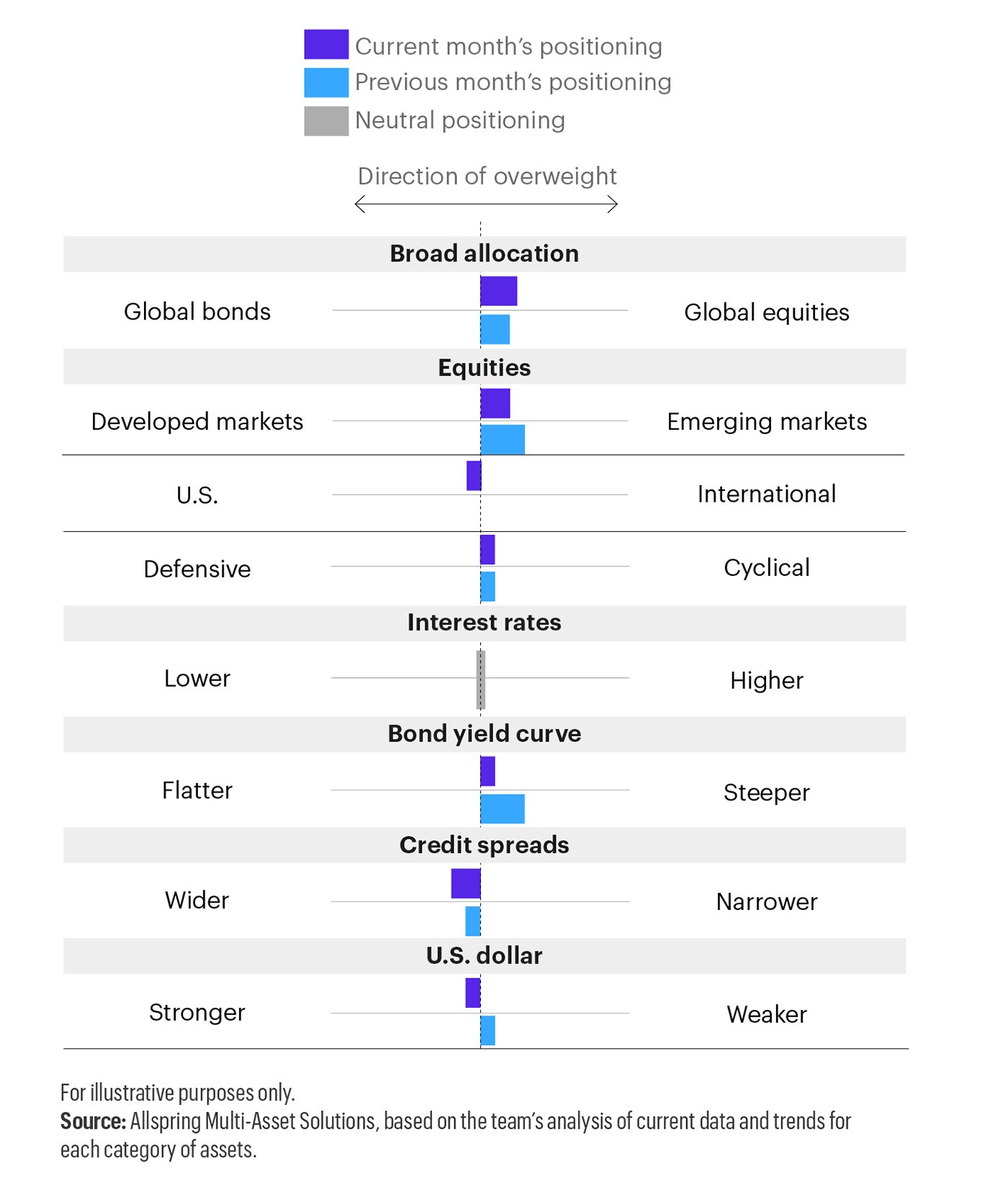

Potential allocations based on today’s environment

The table below depicts our views on short-term trends. These perspectives are developed using quantitative analysis of data over the past 30 years overlaid with qualitative analysis by Allspring investment professionals. The positioning of each bar in the table shows the direction and magnitude of an overweight.

Atlanta Fed’s GDPNow: The Atlanta Fed’s GDPNow is a forecasting model that provides a "nowcast" of the official estimate prior to its release by estimating GDP growth using a methodology similar to the one used by the US Bureau of Economic Analysis.

Consumer Price Index: The Consumer Price Index is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services. You cannot invest directly in an index.

This material is provided for informational purposes only and is intended for retail public distribution in the United States. Use outside the United States is for professional/qualified investors only.

ALL-10312025-qsa4vpst

Related insights

The Federal Reserve (Fed) once again held rates steady against a mixed backdrop of elevated inflation, a weaker labor market, and stable growth (for now). Amid rising geopolitical risk, time will tell how U.S. fundamentals are affected.

Which macroeconomic trends do we think matter the most? Read through the investment implications in this month’s issue of Macro Matters.

Article

Market Impacts: Iran ConflictJoint U.S.-Israeli attacks on Iran over the weekend have sparked a conflict that could draw in much of the Middle East. Explore the short- and long-term implications for investors.

Which macroeconomic trends do we think matter the most? Read through the investment implications in this month’s issue of Macro Matters.

The Federal Reserve (Fed) held rates steady amid solid growth and sticky inflation, with markets reassessing rate-cut expectations as rising commodities, a weaker USD, and political uncertainty complicate the outlook.

Article

Macro Matters: Carry OnWhich macroeconomic trends do we think matter the most? Read through the investment implications in this month’s issue of Macro Matters.

Venezuela's political transition sparks global market ripples, boosting gold and the U.S. dollar while raising questions about oil production, regional politics, and global power dynamics. Explore the short- and long-term implications for investors.

Article

A Fine BalanceThe Federal Open Market Committee (FOMC) dropped its key interest rate by 0.25% to 3.50–3.75%. Going into 2026, we see signs that fiscal stimulus will be more meaningful in addressing the current weakening labor market.

Allspring PMs keep their fingers on the pulse of the markets—and their selfie cameras—going into 2026.

George Bory and Ann Miletti share Allspring's 2026 outlook. From resilient bond strategies to AI-powered equity growth, they unpack the key drivers set to shape next year's financial markets.

Article

Nothing to See HereDespite limited access to reliable data due to the ongoing government shutdown, the Federal Open Market Committee (FOMC) announced another 0.25% cut, lowering its key interest rate to 3.75–4.00%.

How are Allspring’s investment experts thinking about the U.S. government shutdown and market implications?

Macro Matters provides a concise, comprehensive look at macroeconomic themes that matter to clients.

The Federal Reserve lowered its key rate by 25 basis points at its September meeting following an eight-month pause. George Bory and John Campbell discuss how U.S. bond and equity markets could respond.

Macro Matters provides a concise, comprehensive look at macroeconomic themes that matter to clients.

Macro Matters provides a concise, comprehensive look at macroeconomic themes that matter to clients.

With a robust U.S. economy, above-target inflation, and continued tariff uncertainty, the FOMC kept its key interest rate at 4.25–4.50%.

Macro Matters provides a concise, comprehensive look at macroeconomic themes that matter to clients.

Speculation over the next chair of the Federal Reserve (Fed) is dominating headlines and keeping markets on edge. A more dovish leader could mean a big shift in monetary policy and raise concerns about the Fed’s independence.

As the events concerning Iran continue, Allspring Fixed Income’s message—"bonds provide certainty in an uncertain world”—remains central to our positioning.

A potential conflict with Iran has consistently appeared in our monthly Market Risk Monitor for over two years. Now that risk has materialized. Our equity portfolio managers assess the implications for global markets.

What might the future hold for markets? In this roundtable discussion, our investment experts explore pressing topics like deficit spending, trade tensions, the Fed’s next moves, and the weakening U.S. dollar.

With ongoing tariff uncertainty and U.S. employment still strong, the Fed kept its key interest rate at 4.25–4.50%.

Amid uncertainty around tariffs and their impact on U.S. growth and inflation, the Federal Reserve held its key interest rate at 4.25–4.50%. We explain what may lie ahead.