Macro Matters: Fed to Restart Cutting Cycle

Macro Matters provides a concise, comprehensive look at macroeconomic themes that matter to clients.

Key takeaways

- Growth: Global growth will likely stabilize, driven by looser fiscal and monetary policies.

- Inflation: Tariff uncertainty will remain, but slowing fundamentals should gradually bring inflation down.

- Rates: We expect the Federal Reserve (Fed) to cut rates in September by 50 basis points (bps; 100 bps equal 1.00%).

Growth: Fiscal stimulus might partly offset tariff uncertainty

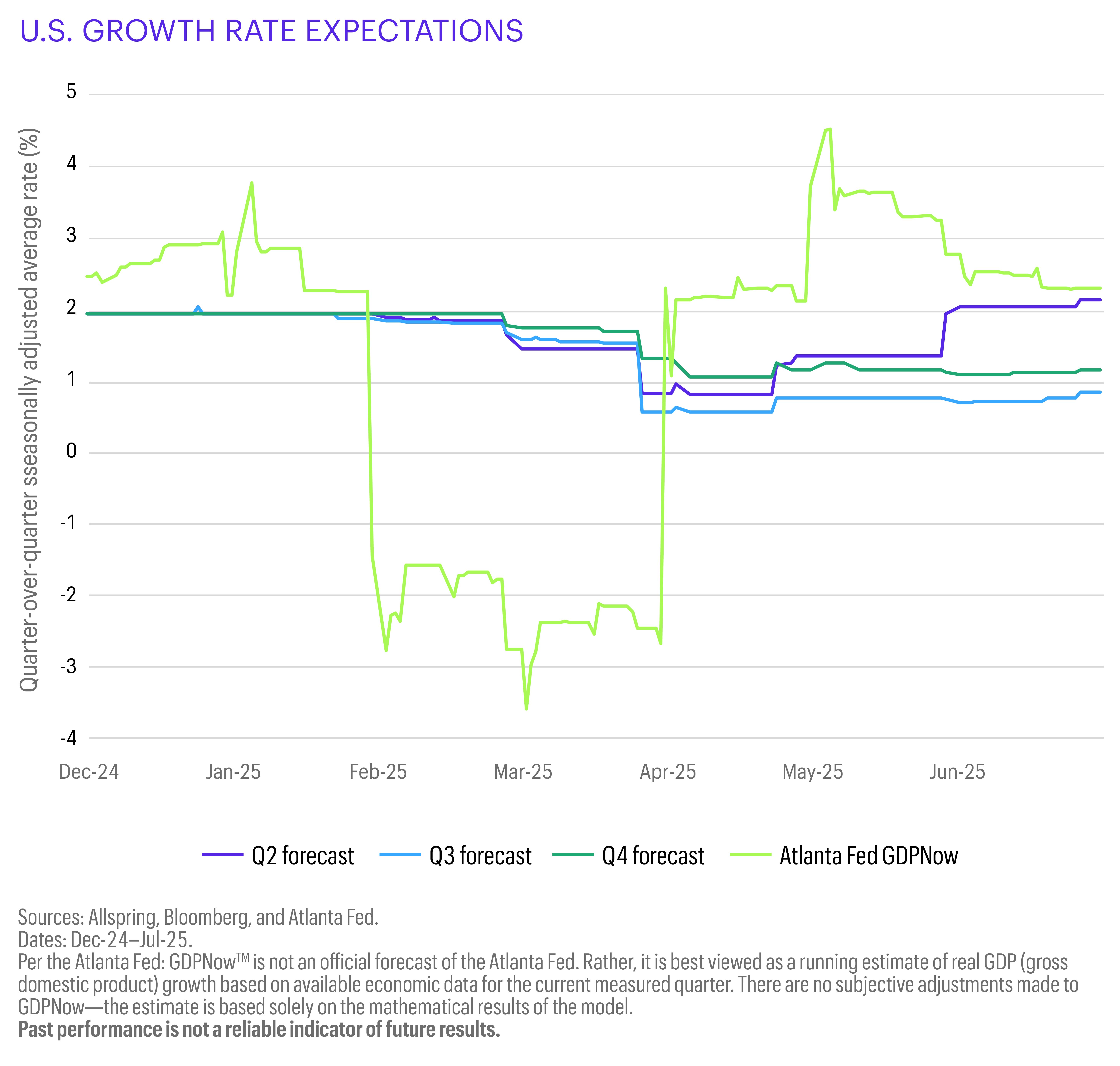

The U.S. economy continues to slow, with a 1.5–2.0% increase expected for the third quarter, according to the Federal Reserve Bank of Atlanta (Atlanta Fed). Survey indicators indicate stabilization in the services sector, while the manufacturing sector continues to struggle with elevated interest rates and the secondary impacts from tariff agreements as they are announced. While U.S. consumers’ mood has stabilized over the summer, we expect continued uncertainty amid slowing in the labor market. The latest nonfarm payrolls were weaker than expected, and revisions to previous months’ readings indicated the weakest pace of job growth since the onset of the pandemic. While fiscal stimulus may be able to offset some of that uncertainty, corporations will be cautious on hiring and consumers will likely increase savings rather than spend. The U.S. managed to announce trade deals with major economies like Japan, the U.K., and the eurozone and has made progress with China. Many details are missing, though, and sectoral tariffs might replace country-specific measures. The tariff impact is negative for both U.S. and international growth.

In the eurozone, we expect economic growth to remain low although some stabilization through increased fiscal stimulus and lower interest rates can be seen. Service sector data show some improvement, and the latest tariff agreement with the U.S. should provide some positive news for the manufacturing sector—although sectoral tariffs for steel and autos could hit the eurozone hard. The European Central Bank (ECB) paused rates for now, but with prices back to target and growth sluggish, we believe more stimulus will be needed to support growth.

China’s second-quarter growth data was in line with the country’s 5% growth target for 2025. Exports showed a nice recovery, and manufacturing displayed some improvement. Any tariff-related relief, however, is likely to be short term. Deflationary forces persist, and China’s property market continues to struggle. The focus remains on boosting domestic consumption, and we believe more stimulus is likely.

Inflation: Tariffs have been keeping inflation sticky for now

U.S. core inflation ticked up slightly in June, from 2.8% to 2.9%. While service sector inflation has been pushing inflation down, goods inflation has risen lately, largely due to the tariffs that had been announced up to that point. Market-based inflation expectations remain stable, and consumers’ one-year-ahead expectations declined from June’s 5.0% to 4.4% in July. However, input cost indicators, such as the Institute for Supply Management Prices Index, remain elevated, suggesting potential short-term pass-through risks. With tariff negotiations making progress, some stabilization is likely over the coming months. In terms of further interest rate cuts, Fed Chair Powell has reiterated a cautious stance that balances inflation control with signs of softening growth.

In the eurozone, inflation hovers around the ECB’s 2.0% target, supported by a stronger euro. The ECB has paused its interest-rate-cutting cycle for now in order to assess the effect of year-to-date cuts on economic growth. Since February, inflation has continued rising in the wake of tax hikes and higher minimum wages that businesses blame for the higher prices. Food inflation rose 4.4% in June. The Bank of England remains cautious, with inflation still sticky. In China, prices remain very low and headline inflation is barely above 0%. The country remains in deflation, reflecting weak domestic demand and persistent property sector slowdown.

Rates: The Fed will likely restart its cutting cycle with a bigger 50-bp cut

The Fed remained on hold in July, keeping the federal funds rate at 4.25–4.50%. While the U.S. inflation trend has moderated, it’s still above target—and over the short term, it may rise due to higher import prices and a weaker U.S. dollar. In our view, tariff uncertainty and a more cautious private sector will lead to lower economic growth, resulting in a 50-bp rate cut in September. Similar to last year when the Fed started cutting rates, its focus will switch back to growth. Weaker growth is likely to outweigh short-term sticky inflation. We expect a total of three rate cuts this year in order to avoid a U.S. recession.

In the eurozone, the ECB has cut rates by 2.00% since early 2024, bringing the deposit rate to 2.00%. For now, the ECB is on hold to assess how much support the latest cuts will provide. The market is expecting one more cut by year-end, which looks realistic to us given lower growth prospects. The Bank of England (BoE) has reduced rates from a peak of 5.25% to the current 4.25%, with markets pricing in two more cuts by year-end. However, with U.K. inflation still above target at 3.6%, the BoE is likely to proceed cautiously in order to support growth.

In China, we expect the People’s Bank of China to continue easing to counter deflation and weak domestic demand. With China’s Consumer Price Index at +0.1%, further rate cuts and targeted lending programs could support growth and stabilize the property sector. Tariff negotiations are ongoing. While some kind of agreement will be found, the pressure on China to rebalance its economy will persist—not just from the U.S., but also from the eurozone and other countries.

Implications for fixed income

While progress has been made in tariff negotiations, many details are missing, and country-specific tariffs will be replaced by sectoral tariffs. Bond markets will be increasingly focusing on fundamentals and on how fiscal stimulus and higher interest rates will affect growth and inflation. In the U.S., growth is likely to slow further as businesses and consumers remain cautious. Yields remain attractive overall, and international central banks will likely resume interest rate cuts after a summer pause. The Fed will likely remain on hold until September and then restart its interest-rate-cutting cycle with a bigger cut.

We believe U.S. bonds will remain supported and earn the carry. Interest rates will likely continue falling on the short end of the curve. Increased fiscal stimulus and a weaker U.S. dollar could lead to more volatility in longer-maturity bonds while short- to medium-term bonds remain attractive. We favor higher-quality U.S. bonds with low- to medium-term durations that are less affected by interest rate and growth volatility.

International bonds remain supported by lower growth and inflation. We’ll need to see the full fiscal effects and the tariff impact, which will likely remain challenging for exports. For now, we remain positive on international bonds given stronger currencies and positive inflation developments.

Implications for equities

We remain modestly positive on equities overall—primarily emerging markets and cheaper sectors of the U.S. market. Valuations are no longer cheap, but earnings momentum remains positive. We see tariff negotiations having a strong impact at the sector level, although overall earnings growth for the second quarter has remained robust at 8%. Slowing growth will likely affect earnings momentum, and we’re seeing this impact in analysts’ slowing earnings expectations for the rest of 2025. Fiscal and renewed monetary stimulus should provide some support, although we expect higher volatility going into the third quarter.

We expect global equity markets to continue to perform mildly positively—including emerging markets—supported by lower real rates, stable earnings momentum, and more Chinese stimulus. Focusing on quality and valuation remains a prudent approach for us.

Implications for multi-asset portfolios

From a multi-asset perspective, we maintain a constructive view on global equities, particularly in Europe, emerging markets, and China, where valuations remain attractive and trade sentiment has begun improving. Within the U.S., we prefer sectors less affected by tariffs, like technology. We expect the Fed’s eventual pivot toward growth support to bolster equity sentiment later this year through bigger interest rate cuts.

We continue to like bonds over cash. In the U.S., we believe the interest rate curve has room to steepen. With the Fed gradually expected to shift from inflation to growth support in the second half of 2025, U.S. equities should benefit from lower interest rates, fiscal stimulus, and waning tariff concerns. Tariffs are, however, here to stay and could potentially create short-term uncertainties through sectoral tariffs. We remain underweight the U.S. dollar given the outlook for lower interest rates in the U.S., and we prefer gold as a diversifier.

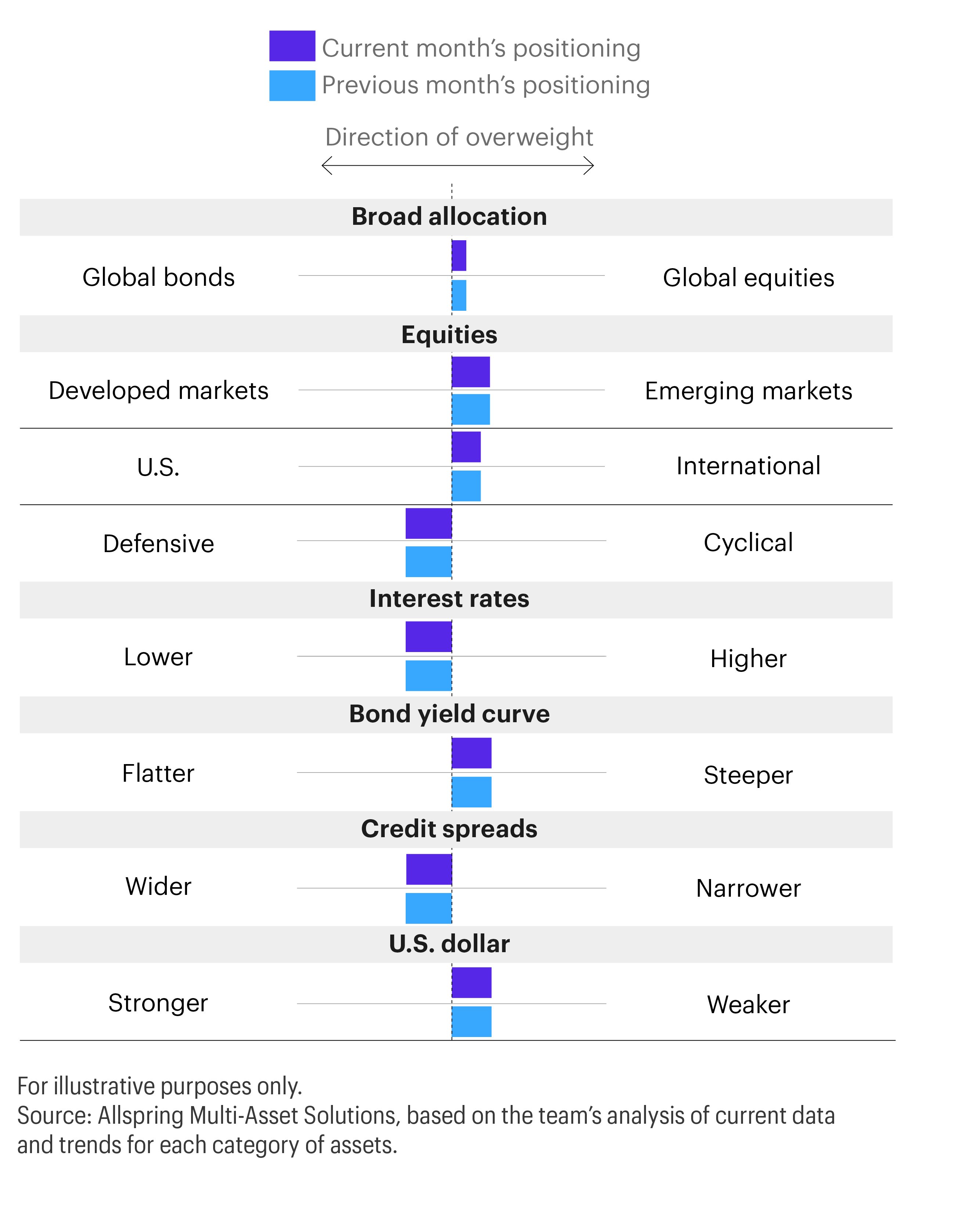

Potential allocations based on today’s environment

The table below depicts our views on short-term trends. These perspectives are developed using quantitative analysis of data over the past 30 years overlaid with qualitative analysis by Allspring investment professionals. The positioning of each bar in the table shows the direction and magnitude of an overweight.

This material is provided for informational purposes only and is intended for retail public distribution in the United States. Use outside the United States is for professional/qualified investors only.

ALL-08052025-39ps1oxn

Related insights

Which macroeconomic trends do we think matter the most? Read through the investment implications in this month’s issue of Macro Matters.

The Federal Reserve (Fed) once again held rates steady against a mixed backdrop of elevated inflation, a weaker labor market, and stable growth (for now). Amid rising geopolitical risk, time will tell how U.S. fundamentals are affected.

Which macroeconomic trends do we think matter the most? Read through the investment implications in this month’s issue of Macro Matters.

Article

Market Impacts: Iran ConflictJoint U.S.-Israeli attacks on Iran over the weekend have sparked a conflict that could draw in much of the Middle East. Explore the short- and long-term implications for investors.

Which macroeconomic trends do we think matter the most? Read through the investment implications in this month’s issue of Macro Matters.

The Federal Reserve (Fed) held rates steady amid solid growth and sticky inflation, with markets reassessing rate-cut expectations as rising commodities, a weaker USD, and political uncertainty complicate the outlook.

Article

Macro Matters: Carry OnWhich macroeconomic trends do we think matter the most? Read through the investment implications in this month’s issue of Macro Matters.

Venezuela's political transition sparks global market ripples, boosting gold and the U.S. dollar while raising questions about oil production, regional politics, and global power dynamics. Explore the short- and long-term implications for investors.

Article

A Fine BalanceThe Federal Open Market Committee (FOMC) dropped its key interest rate by 0.25% to 3.50–3.75%. Going into 2026, we see signs that fiscal stimulus will be more meaningful in addressing the current weakening labor market.

Allspring PMs keep their fingers on the pulse of the markets—and their selfie cameras—going into 2026.

George Bory and Ann Miletti share Allspring's 2026 outlook. From resilient bond strategies to AI-powered equity growth, they unpack the key drivers set to shape next year's financial markets.

Which macroeconomic trends do we think matter the most? Read this month’s issue of Macro Matters.

Article

Nothing to See HereDespite limited access to reliable data due to the ongoing government shutdown, the Federal Open Market Committee (FOMC) announced another 0.25% cut, lowering its key interest rate to 3.75–4.00%.

How are Allspring’s investment experts thinking about the U.S. government shutdown and market implications?

Macro Matters provides a concise, comprehensive look at macroeconomic themes that matter to clients.

The Federal Reserve lowered its key rate by 25 basis points at its September meeting following an eight-month pause. George Bory and John Campbell discuss how U.S. bond and equity markets could respond.

Macro Matters provides a concise, comprehensive look at macroeconomic themes that matter to clients.

With a robust U.S. economy, above-target inflation, and continued tariff uncertainty, the FOMC kept its key interest rate at 4.25–4.50%.

Macro Matters provides a concise, comprehensive look at macroeconomic themes that matter to clients.

Speculation over the next chair of the Federal Reserve (Fed) is dominating headlines and keeping markets on edge. A more dovish leader could mean a big shift in monetary policy and raise concerns about the Fed’s independence.

As the events concerning Iran continue, Allspring Fixed Income’s message—"bonds provide certainty in an uncertain world”—remains central to our positioning.

A potential conflict with Iran has consistently appeared in our monthly Market Risk Monitor for over two years. Now that risk has materialized. Our equity portfolio managers assess the implications for global markets.

What might the future hold for markets? In this roundtable discussion, our investment experts explore pressing topics like deficit spending, trade tensions, the Fed’s next moves, and the weakening U.S. dollar.

With ongoing tariff uncertainty and U.S. employment still strong, the Fed kept its key interest rate at 4.25–4.50%.