Macro Matters: Tariff Uncertainty Taking a Toll

Macro Matters provides a concise, comprehensive look at macroeconomic themes that matter to clients.

Key takeaways

- Growth: Continued global weakening driven by tariff uncertainty

- Inflation: Tariff-induced stickier U.S. inflation and lower international inflation

- Rates: Federal Reserve (Fed) on hold longer than market expects—internationally, more cuts

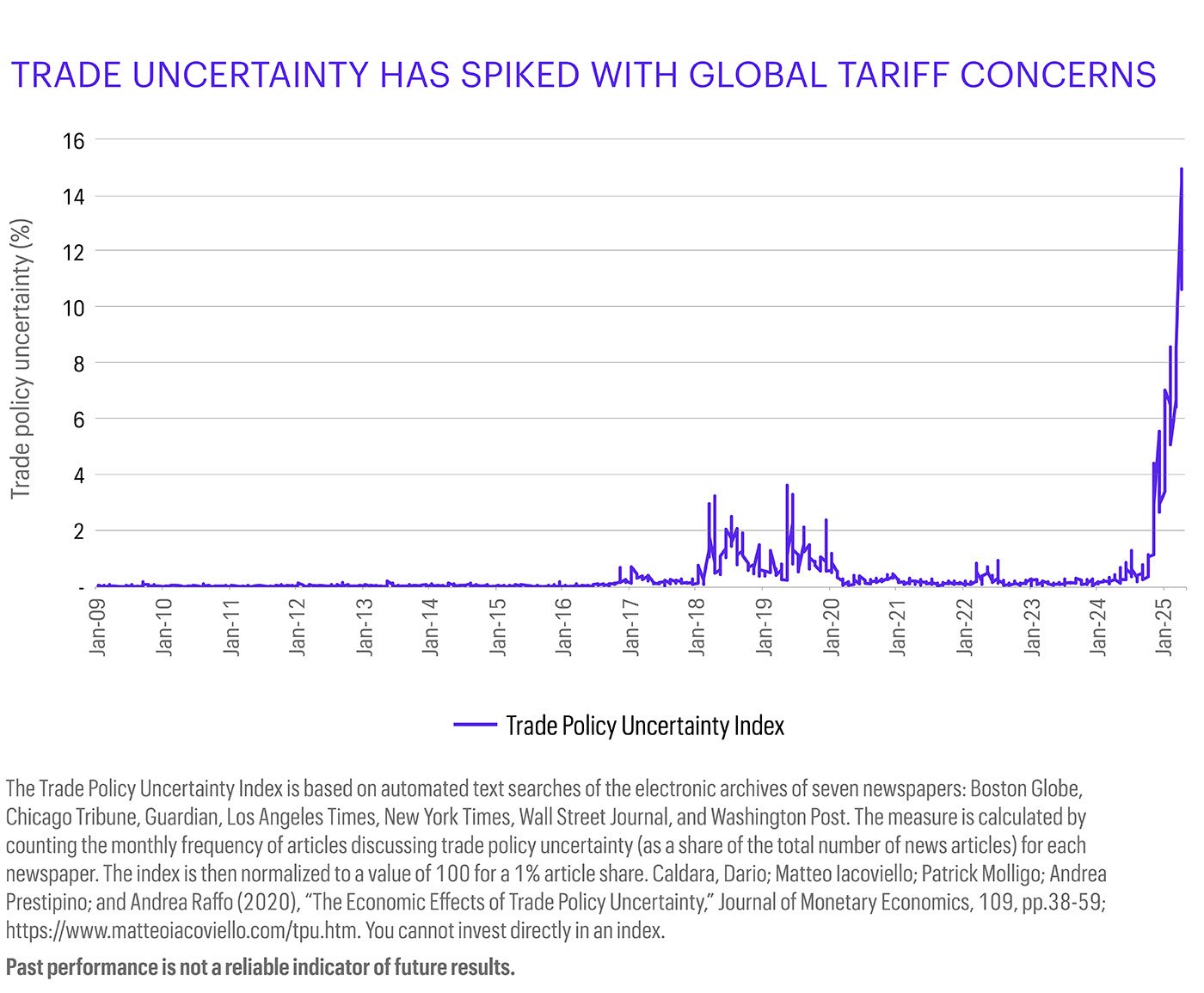

Growth: Tariff uncertainty likely to weigh on growth

Before the tariff increases began, many companies started front-loading imports into the U.S. This has likely boosted activity globally in the short term, though the impact should fade quickly. The latest higher-frequency sentiment indicators point to weakening activity in manufacturing and services. Real gross domestic product (GDP) will likely be significantly negatively affected by commodity and other imports ahead of the tariff announcements, and the medium-term trend also indicates further slowing. Tariffs’ negative impacts are felt beyond the manufacturing sector as the latest technology company exemptions reveal the vulnerability of U.S. mega-cap companies that have outsourced production to low-cost countries.

Although the U.S. labor market has remained resilient thus far, consumer sentiment has dropped sharply and consumers’ latest inflation expectations have reached a level last seen in the early 1980s. This clearly has the potential to weigh on consumer spending. The latest rhetoric around the Fed’s independence is not helpful to growth sentiment: Riskier assets as well as bonds have reacted negatively to comments about removing Fed Chair Powell from his role early. Monetary policy is not likely to help with lower interest rates for now—hence, there’s more pressure on fiscal stimulus. That said, the U.S. budget situation is not great and bond vigilantes’ upward pressure on bond yields has made mortgages more expensive, with the average 30-year U.S. mortgage rate close to 7.0%.

Internationally, tariffs are likely to put downward pressure on growth and inflation. Global GDP will likely drop from 3.1% to 2.7%. Export-driven nations will be affected the most. Germany’s investor confidence has plummeted lately, as exports are likely to take a hit under the current tariff regime. Negotiations are ongoing and announced tariffs might come down, although uncertainty continues to negatively affect investors’ and consumers’ sentiment. Looser fiscal policy and more rate cuts can likely provide some support, although tariffs’ impact is disinflationary through an external demand shock for exports. Increased domestic demand probably won’t offset the loss of exports, and consumers are likely to save more than they consume.

China’s first-quarter growth data have been robust, though real GDP growth will likely drop from 5.0% to 0.8% in the second quarter given that current tariffs make exports to the U.S. very difficult and other nations will try to prevent re-routing of China’s exports from the U.S. into their home markets.

Inflation: U.S. stagflation versus disinflation internationally

The latest U.S. inflation reading has surprised on the downside, though a short-term boost toward 3% in the Fed’s preferred consumption-based inflation measure is likely under the current tariff regime. Market-based inflation gauges remain well behaved. However, both consumer expectations and indicators such as the Institute for Supply Management Prices Index have risen sharply lately, pointing to increased uncertainty regarding inflation expectations. Several Fed members, including Fed Chair Powell, have noted that this situation warrants a more cautious Fed approach. While weaker growth and falling commodity prices could help bring inflation down over the medium term, the short-term impact of tariff-induced price increases and a weaker U.S. dollar could be significant.

Outside the U.S., eurozone inflation remains close to target and the European Central Bank (ECB) continued cutting interest rates. More downward pressure is likely, helped by falling commodity prices and a stronger euro. European growth will likely slow due to the additional tariffs. China remains at the center of U.S. tariffs, and weaker growth ahead is pressuring prices further downward. China’s latest inflation readings confirmed regression into deflation before the tariffs even hit.

Rates: Fed on hold until autumn

The Fed remains in a tough spot. While underlying inflation has been easing, the outlook remains highly uncertain due to tariffs’ impact on consumers’ price expectations. Rates are reasonably restrictive, and the Fed is likely to hold over the summer to see the degree of impact the tariffs have on inflation and growth. In contrast, the interest market expects up to four rate cuts this year based on much weaker growth forecasts, while the Fed itself projects two. There is plenty of room for disappointment.

In April, we saw a large divergence in global bond performance. While international bonds rallied strongly and generated a return over 5%, the U.S. 10-year Treasury declined by 1%. Disinflation internationally—versus stagflation prospects in the U.S. and a careful Fed—led to the divergence. We believe the divergence was triggered not by foreign institutions selling U.S. Treasury bonds but rather by the cloudier growth outlook in the U.S. that raises questions about the long-term sustainability of the U.S. debt level and financing of further fiscal stimulus efforts. On the international side, we expect at least three more rate cuts by both the ECB and the Bank of England as both growth and inflation continue to weaken. Also, China is likely to ramp up fiscal and monetary loosening to shield its economy from the tariffs’ impact.

Implications for fixed income

With increasing global trade uncertainty, bonds should benefit from questions about growth. Yields remain attractive overall, and international central banks are likely to cut more aggressively compared with expectations set at the beginning of 2025. The Fed will likely remain on hold, which supports current attractive real yields.

We believe U.S. bonds will remain supported and earn the carry despite recent volatility and underperformance. Interest rates will likely continue falling on the short end of the curve, though probably not before the third quarter of 2025. Farther out on the curve, there’s likely more interest rate volatility ahead because tariffs can potentially increase inflation through higher import prices and a possibly weaker U.S. dollar. We expect the interest rate curve to continue steepening as the market rebuilds a term premium into long-maturity bonds. We favor higher-quality U.S. bonds with low- to medium-term durations that are less affected by interest rate and growth volatility.

International bonds remain supported by lower growth and inflation, although this is largely priced in already. We’ll need to see the full effects of the fiscal stimulus through defense spending and how much of it will drive personal consumption higher, rather than the savings rate. We remain positive on international bonds for now.

Implications for equities

We remain cautious on equities overall and continue to expect a shift away from tech-focused U.S. equities toward more diversified international equities. A weaker U.S. dollar and lower rates internationally combined with the expected negative impact of U.S. trade tariffs on U.S. consumers have led to international equities’ outperformance. Potentially lower geopolitical risk could boost international stock markets and more fiscal spending could boost U.S. equities. Ongoing tariff spats, though, could likely trigger more equity market volatility. Inflation could decline further later this year and provide some support for U.S. equities, although shorter-term uncertainties could continue dominating price action.

We expect the global equity market’s broadening to continue—including emerging markets supported by cheaper valuations, lower real rates, weaker currencies, and more Chinese stimulus. Focusing on quality and valuation remains a prudent approach for us.

Implications for multi-asset portfolios

Since the beginning of 2025, we’ve been adding to our international equity exposure while reducing U.S. equity exposure. European, emerging market, and Chinese equities offer good diversification in a more volatile market environment. We continue to like bonds over cash, especially on the international side. In the U.S., we believe the interest rate curve has further room to steepen. With the Fed more focused on inflation concerns than on lower growth, U.S. asset volatility is likely to stay higher. Tariff concerns will likely keep introducing short-term volatility. We remain underweight the U.S. dollar and overweight gold given the increased likelihood of trade tariffs triggering negative side effects on growth and inflation.

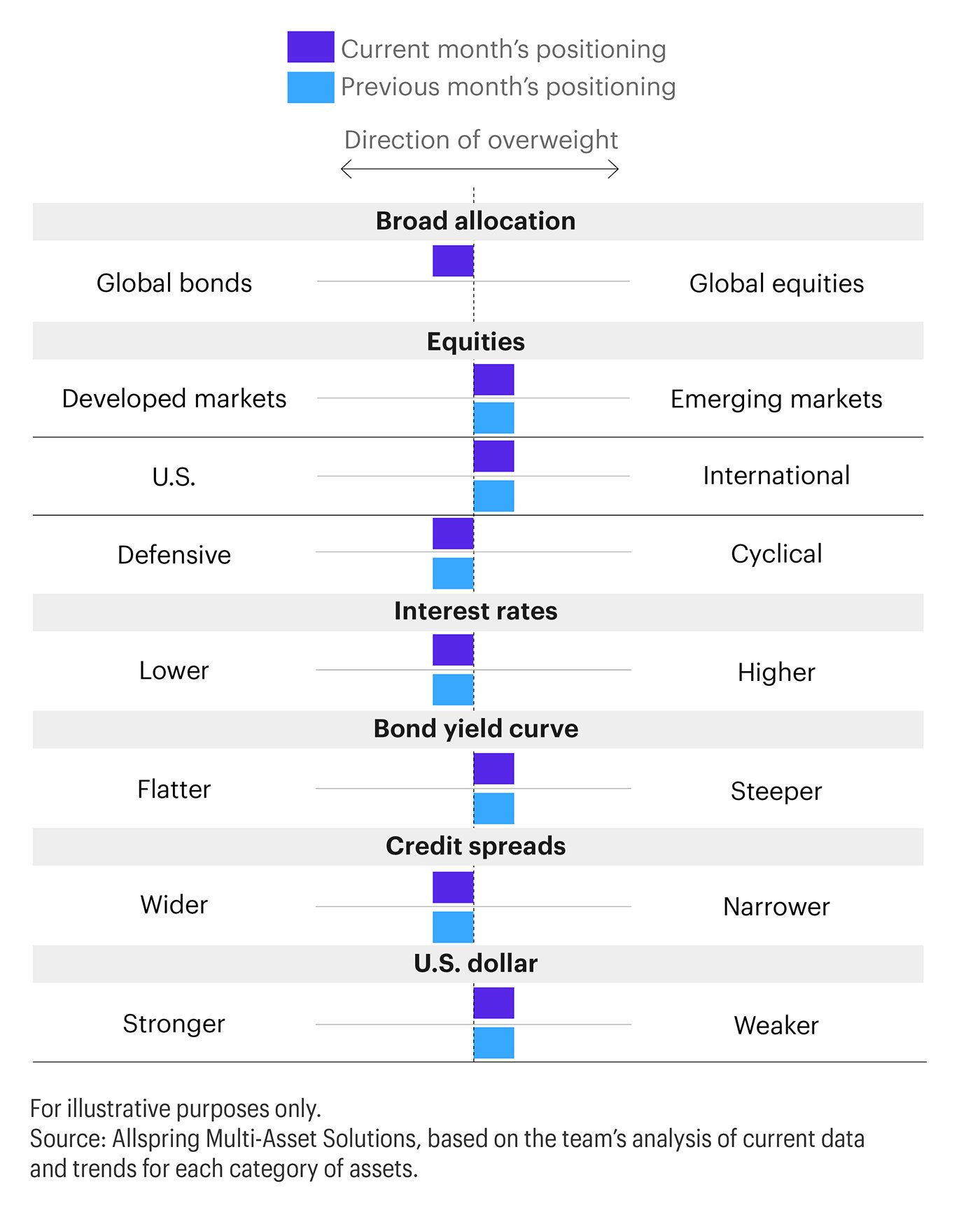

Potential allocations based on today’s environment

The table below depicts our views on short-term trends. These perspectives are developed using quantitative analysis of data over the past 30 years overlaid with qualitative analysis by Allspring investment professionals. The positioning of each bar in the table shows the direction and magnitude of an overweight.

This material is provided for informational purposes only and is intended for retail public distribution in the United States. Use outside the United States is for professional/qualified investors only.

ALL-04292025-4mzdq3u6

Related insights

Which macroeconomic trends do we think matter the most? Read through the investment implications in this month’s issue of Macro Matters.

The Federal Reserve (Fed) once again held rates steady against a mixed backdrop of elevated inflation, a weaker labor market, and stable growth (for now). Amid rising geopolitical risk, time will tell how U.S. fundamentals are affected.

Which macroeconomic trends do we think matter the most? Read through the investment implications in this month’s issue of Macro Matters.

Article

Market Impacts: Iran ConflictJoint U.S.-Israeli attacks on Iran over the weekend have sparked a conflict that could draw in much of the Middle East. Explore the short- and long-term implications for investors.

Which macroeconomic trends do we think matter the most? Read through the investment implications in this month’s issue of Macro Matters.

The Federal Reserve (Fed) held rates steady amid solid growth and sticky inflation, with markets reassessing rate-cut expectations as rising commodities, a weaker USD, and political uncertainty complicate the outlook.

Article

Macro Matters: Carry OnWhich macroeconomic trends do we think matter the most? Read through the investment implications in this month’s issue of Macro Matters.

Venezuela's political transition sparks global market ripples, boosting gold and the U.S. dollar while raising questions about oil production, regional politics, and global power dynamics. Explore the short- and long-term implications for investors.

Article

A Fine BalanceThe Federal Open Market Committee (FOMC) dropped its key interest rate by 0.25% to 3.50–3.75%. Going into 2026, we see signs that fiscal stimulus will be more meaningful in addressing the current weakening labor market.

Allspring PMs keep their fingers on the pulse of the markets—and their selfie cameras—going into 2026.

George Bory and Ann Miletti share Allspring's 2026 outlook. From resilient bond strategies to AI-powered equity growth, they unpack the key drivers set to shape next year's financial markets.

Which macroeconomic trends do we think matter the most? Read this month’s issue of Macro Matters.

Article

Nothing to See HereDespite limited access to reliable data due to the ongoing government shutdown, the Federal Open Market Committee (FOMC) announced another 0.25% cut, lowering its key interest rate to 3.75–4.00%.

How are Allspring’s investment experts thinking about the U.S. government shutdown and market implications?

Macro Matters provides a concise, comprehensive look at macroeconomic themes that matter to clients.

The Federal Reserve lowered its key rate by 25 basis points at its September meeting following an eight-month pause. George Bory and John Campbell discuss how U.S. bond and equity markets could respond.

Macro Matters provides a concise, comprehensive look at macroeconomic themes that matter to clients.

Macro Matters provides a concise, comprehensive look at macroeconomic themes that matter to clients.

With a robust U.S. economy, above-target inflation, and continued tariff uncertainty, the FOMC kept its key interest rate at 4.25–4.50%.

Macro Matters provides a concise, comprehensive look at macroeconomic themes that matter to clients.

Speculation over the next chair of the Federal Reserve (Fed) is dominating headlines and keeping markets on edge. A more dovish leader could mean a big shift in monetary policy and raise concerns about the Fed’s independence.

As the events concerning Iran continue, Allspring Fixed Income’s message—"bonds provide certainty in an uncertain world”—remains central to our positioning.

A potential conflict with Iran has consistently appeared in our monthly Market Risk Monitor for over two years. Now that risk has materialized. Our equity portfolio managers assess the implications for global markets.

What might the future hold for markets? In this roundtable discussion, our investment experts explore pressing topics like deficit spending, trade tensions, the Fed’s next moves, and the weakening U.S. dollar.