Shifting the Mix: How Insurers Are Reallocating Bond Portfolios

With dramatic shifts within fixed income from 2022–2024, insurers gradually reallocated, seeking better opportunities. We explore how successful insurer allocations may look going forward.

Authors

-

Ed Martin, CFA

8/18/2025

5 min read

Topic

Fixed Income

Key takeaways

- Following insurers’ allocation shifts between 2022 and 2024, we analyzed the growth in bond market subsectors and identified clear trends.

- We believe the allocation shifts we found reflect insurers’ reactions to past performance as well as their expectations for future bond subsector results.

- Several Allspring senior portfolio managers provide their views on current insurer fixed income allocations and what they would emphasize going forward.

Introduction

Each spring, the release of detailed statutory data on insurance company bond holdings offers a window into how insurers are positioning their portfolios. In the wake of the sharp interest rate increases that began in 2022, the investment landscape for fixed income investors shifted dramatically. Short-term rates surged from pandemic-era lows, and the long-standing environment of rate suppression gave way to a more volatile and yield-rich market.

While many companies were reluctant to realize capital losses on existing holdings, they gradually reallocated capital toward sectors offering better value, stronger credit fundamentals, or more favorable capital treatment. But are these trends the right choice for the future? We asked some of Allspring’s senior portfolio managers whether these trades looked good in retrospect and what they would emphasize in the future.

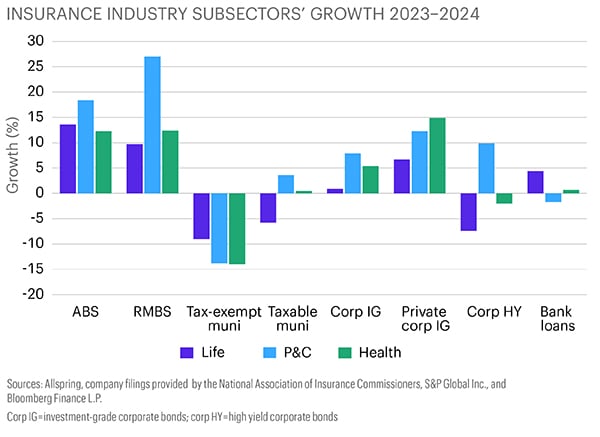

Our analysis of year-end bond holdings from 2022 through 2024 reveals several clear trends. Residential mortgage-backed securities (RMBS) saw the most significant rise in allocations, particularly among property & casualty (P&C) insurers, reflecting a growing appetite for high-quality, yield-enhanced assets with favorable convexity profiles. Asset-backed securities (ABS) also gained ground across all sectors, supported by their relative liquidity and capital efficiency.

Conversely, allocations to tax-exempt and taxable municipal bonds (munis) declined across the board, likely reflecting both regulatory headwinds and relative value considerations.

The chart below shows growth in bond market subsectors over 2023 and 2024. For example, the P&C industry’s RMBS grew at a 27% annualized rate from year-end 2022 to year-end 2024.

The allocation shifts aren’t just reactions to past performance—they reflect forward-looking views on credit quality, liquidity, and interest rate volatility. Insights from our portfolio managers suggest that they believe active management and security selection will remain critical in extracting value from sectors like RMBS and ABS, and muni sectors may warrant a closer look.

ABS: yield, liquidity, and capital efficiency

ABS allocations increased across all three insurance sectors, with life insurers leading the way. The appeal of ABS lies in its ability to deliver spread over similarly rated corporates, often with shorter duration and higher credit quality.

Mira Park, senior portfolio manager on Allspring’s Investment Grade Income team, noted that while spreads have compressed, ABS remain cheap relative to corporates and the sector continues to offer value. This is especially evident in newer subsectors like digital infrastructure and unsecured consumer credit—with spreads up to 100 basis points (bps; 100 bps = 1.00%) over similarly rated corporates, they’re attractive to insurers with intermediate-duration liabilities.

“We’ve been a proponent of off-the-run esoteric ABS for over a decade,” Park said. “Spreads have not tightened as much as corporates, so ABS are cheap at the moment on a relative basis. But importantly, all-in yields are pretty high versus the historical averages, which is very attractive to insurers.” Park also emphasized that the average credit quality of the ICE BofA U.S. Fixed Rate Miscellaneous ABS Index is AA- and some structures amortize from day one, providing natural deleveraging. “These structures proved very resilient, even through onerous financial disruptions like COVID, where we saw downgrades in just a few select subsectors. The average credit quality is high, and liquidity—while not as deep as corporates—is still attractive.”

Performance of the index was strong in 2023 and 2024, showing that insurers were wise to allocate to this sector. The sector’s diversity—from data centers to consumer finance—offers ample room for portfolio customization, making it a natural fit for insurers.

RMBS: a reemerging core

Among all fixed income sectors, RMBS experienced the most pronounced increase in allocation—particularly within P&C portfolios, where exposure rose by over 20% beyond the growth in the P&C industry. There are many reasons for insurers to emphasize RMBS, including high quality, outstanding liquidity, and more competitive yields.

The post–2022 environment brought a wave of new issuance with higher coupons and more diverse collateral profiles. This created fertile ground for active managers to extract value through security selection. Jarad Vasquez, senior portfolio manager and co-head of Allspring’s Core Fixed Income team, emphasized that since 2022, “RMBS have been an attractive space from a security-selection standpoint. While the mortgage sector as a whole may not have performed as well as others, the ability to generate alpha through security selection has been much greater.”

Vasquez expects this dynamic to continue. As interest rate uncertainty persists, the sector’s sensitivity to prepayment dynamics will likely create opportunities for managers who can navigate the nuances of loan balance, seasoning, and structure. He noted, “I think taking advantage of these dislocations in the market is the biggest opportunity in the agency market, and it's really what differentiates it from some of the other spread sectors in the market right now.”

Municipal bonds: diversification and credit strength

While structured credit has gained favor, one area that has encountered declining allocations is municipal bonds—especially tax-exempt munis. This trend has been driven by changes to the corporate tax code, which reduced the relative benefit of tax-exempt income for corporations, including insurers.

Allspring’s Nicholos Venditti, senior portfolio manager and head of Municipal Fixed Income, believes the market may be overlooking the value of taxable munis: “Taxable munis are starting to look pretty interesting … the yields are roughly equivalent to investment-grade corporates, but they have substantially better credit characteristics.” Regarding munis’ diversification benefit, he said, “There are levels of why it's better. On the surface, it's better because triple B-rated munis default less frequently than triple A-rated corporates do ... and in addition to providing diversification away from other asset classes, there’s a ton of diversification even within the asset class.”

The amount of money that can be easily deployed in the muni market is somewhat constrained by the fact that it has less liquidity than the corporate bond market: While the muni market has far more issuers, it has only about 40% of the outstanding principal that the corporate bond market does. Still, for insurers seeking diversification, the muni sector offers unique benefits. Its low correlation among issuers adds a layer of resilience not found in relatively more homogenous sectors, like corporates or financials.

Credit: Keep an eye on credit fundamentals

The data show a mixed picture for corporate credit. Investment-grade public corporates saw modest increases in holdings, but there was more robust growth in private corporates. This difference reflects a broader trend toward less liquid, higher-yielding alternatives that still meet capital and rating requirements. George Bory, Allspring’s chief investment strategist for Fixed Income, observed, “There was a realization among insurers that if we’re going to be sellers of liquidity, we might as well sell it full stop. Capital is assessed relative to the ratings of a bond, not its liquidity, and if we can get paid more for a given rating by selling liquidity, then we'll take it.”

One area of concern in the credit universe is the loan market. While performance has held up, concerns about rising default rates and deteriorating recovery values—especially in the loan market—have prompted a reevaluation. As Bory noted, “Loan defaults are rising faster than high yield, and recovery rates have dropped from 60–80% to 20–30%. That’s a structural shift.” Here again, strong fundamental credit research is key to solid performance, especially in the face of economic volatility.

Conclusion: a more selective, strategic approach

The past two years have marked a turning point in how insurers allocate capital across the bond market. The message from portfolio managers is clear: In a world of tighter spreads and greater volatility, success will depend not just on sector selection, but also on the ability to identify value within sectors. We believe that active management, credit work, and a willingness to embrace complexity will define the next chapter in insurance asset allocation.

The ICE BofA U.S. Fixed Rate Miscellaneous Asset-Backed Securities (ABS) Index tracks the performance of ABS that are rated AA to BBB and are collateralized by anything other than: auto loans, home equity loans, manufactured housing, credit card receivables, and utility assets. You cannot invest directly in an index.

This material is provided for informational purposes only and is intended for retail public distribution in the United States. Use outside the United States is for professional/qualified investors only.

ALL-08052025-lfrnhv4p

Related insights

George Bory explains why bond markets in 2026 should favor discipline and flexibility. Positive real yields, global policy divergence, and credit dispersion may create opportunities for income generation and selective positioning.

Janet Rilling and Hannah Rosencrantz give a Q3 fixed income market update—discussing strong bond performance, potential risks in credit compensation, and strategies for building resilient portfolios in Q4.

Fixed income benchmark construction has two fundamental flaws. First, exposures prioritize the needs of borrowers rather than investors. Second, this tends to expose investors to the biggest risks at the worst times.

Two of Allspring’s senior portfolio managers and high yield specialists, Chris Lee and Mike Schueller, sit down with Daniel Sarnowski to discuss recent volatility and why focusing on shorter-duration, higher-quality high yield assets could be the answer in uncertain markets.

Nick Venditti, Allspring’s head of Municipal Fixed Income, explains the impact of the recently passed One, Big, Beautiful Bill on our SpringTalk Muni Moments. And the good news for muni investors? It’s not bad news.

After a mid-April “tariff tantrum,” bond markets appear to be moving past trade headlines and turning their attention to upcoming tax policy and budget negotiations.

George Bory, chief investment strategist for Allspring Fixed Income, explains how active investing in fixed income can offer key advantages over passive investing by prioritizing investor needs, accounting for opportunity costs, and exploiting structural inefficiencies within the bond market.

Nick Venditti, head of Municipal Fixed Income, delves into the recent volatility in the fixed income markets in this episode of Allspring Muni Moments. With elevated yields and favorable muni-to-Treasury ratios, Nick highlights why now might be the time to explore municipal fixed income investments.

The market volatility following “Liberation Day” drove municipal yields to levels not seen since the Global Financial Crisis, presenting real opportunities for investors.

Bond markets are adjusting to tariff impacts amid economic uncertainty. Fixed income investments can help protect against downturns. Expect further yield curve steepening and sector rotation. Use “Riding the Curve” solutions to help maximize income and diversify duration.

Nick Venditti, head of Municipal Fixed Income at Allspring Global Investments, talks about how, for the first time in a while, the higher education sector is starting to show signs of distress.

Allspring's Plus Fixed Income team explains the three key elements they believe may lead to a more balanced and enhanced return profile.