Emerging Markets: Navigating the Investment Opportunities from Generative AI

The emergence of Generative Artificial Intelligence (AI) has created a rush of interest from investors hoping to capitalize on the long-term growth opportunity.

Key takeaways

- The emergence of a generative artificial intelligence (AI) ecosystem of hardware and software companies is taking root in emerging markets.

- Hardware companies are among the early beneficiaries of the AI boom in emerging markets while software companies are at an earlier stage of development.

- A balanced mix of companies exposed to the AI boom can provide portfolios with both shorter- and longer-term opportunities along the AI value chain.

Emerging markets—characterized by higher longer-term growth, fast evolving application scenarios, and lower IT spending as a percentage of gross domestic product—offer unique opportunities and challenges for investors seeking exposure to Generative AI. A robust and rapidly developing ecosystem of hardware and software companies may not only dominate this space in emerging markets but also rival players in the developed world.

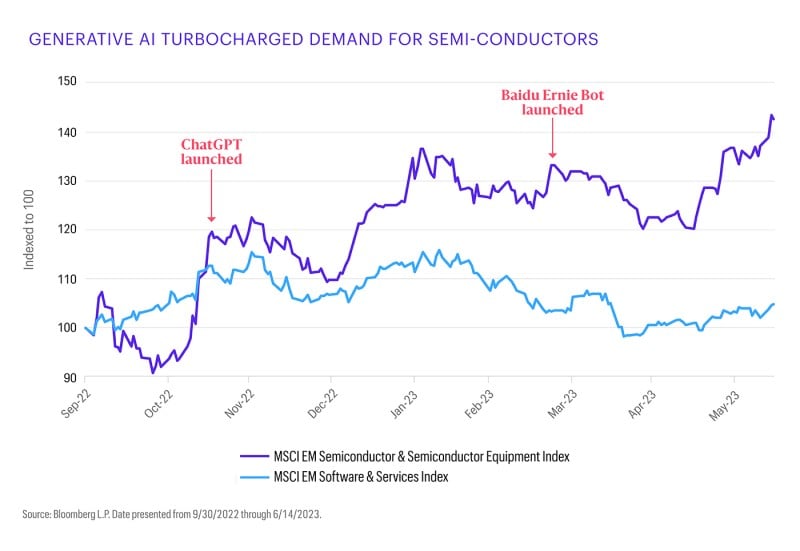

The extensive data size and complexity of large language models (LLMs) require a high-specification, high-cost AI infrastructure. For example, based on industry estimates, an AI training server can cost 15 times more than a general server. Like companies that provided the “picks and shovels” during the 1840s gold rush, companies that have exposure to the hardware supply chain of AI in emerging markets are among the early beneficiaries of the AI boom driven by surging interest in the supply chain. Indeed, like the gold mining industry, having a robust infrastructure in place is a prerequisite for any successful mining operations. Emerging markets have quality hardware companies that can capitalize on these opportunities.

Meanwhile, software and internet companies in emerging markets can be likened to gold miners. These companies develop the algorithms, software platforms, and applications that extract value and insights from the vast amounts of available data. Despite being just as integral to the emerging markets AI ecosystem as the hardware players, the software sector’s year-to-date share price rally has been comparatively lackluster. These software “gold miners” must navigate an emerging market landscape with regulatory, geopolitical, and technological challenges to “strike gold” (i.e., monetize their investment in AI).

Emerging market software and internet companies are at an earlier stage of commercialization of AI Generated Content (AIGC) versus their developed market peers and face more challenges in regulation and procurement of innovative hardware. However, we believe these challenges are reflected in their current valuations, leading them to trade lower than our estimates of their longer-term intrinsic value. As AI continues to grow, we expect leaders to emerge. The sector is worth watching closely because, unlike the actual gold mining industry, where gold miners are constrained by reserves in the ground, the “gold miners” in the AI industry have the potential to operate recurring revenue models that provide a more predictable and stable income stream, resulting in higher value over the life of the investment.

Within our emerging market coverage, we see an increasing number of software and internet companies developing both fundamental LLMs and application layers (using third-party LLMs). On the demand side, despite weak IT spending pickup year to date, we are seeing strong customer interest at business and consumer levels, especially on trailing AIGC services with a strong pipeline of products and demos to be released in the second half of 2023. Moreover, these companies are coming off a lower base in terms of monetization metrics such as user paying ratio, percentage of recurring revenues, and average revenue per user, which implies a longer runway for growth. Emerging markets, which are characterized by higher longer-term growth and evolving market needs, have software and internet companies that can implement, adapt, and upgrade their AI solutions on top of their core functions. These companies can use pricing strategies to drive revenue and earnings growth with government and institutional support providing additional tailwinds.

In sum, we see hardware, software, and internet companies as being integral to the emerging market AI ecosystem with the software and internet companies trading at potentially attractive valuations. By building a balanced mix of these companies at the portfolio level, we can capture the shorter- and longer-term opportunities along the value chain in various aspects of the emerging market AI industry.

Source: MSCI. MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further nredistributed or used as a basis for other indexes or any securities or financial products. This report is not approved, reviewed, or produced by MSCI.

Related insights

Investors face uncertainty around U.S. presidential elections, driving market volatility. How might companies be affected? Have elections affected equity returns long term? Allspring’s Ann Miletti provides perspective.

We discuss two risks investors face: 1) the increased risk in strategies mirroring the S&P 500 as just a few holdings drive its results, and 2) the huge wall of corporate debt maturing in 2025–2029 that will need renewal at much higher rates.

The Special Global Equity team identifies three current market conditions, including U.S. large cap concentration, high but falling inflation, and attractive small-cap stock valuations, and explores why they may signal a comeback for global small-cap stocks.

Income-paying equities—especially those that tend to increase dividends—can help maintain “real return” and stability in a primarily fixed income portfolio.

Our Special Global Equity team explains why they believe U.S. G-SIBs, with more than $150 billion in excess capital, are currently undervalued and regional banks are overvalued relative to their respective risk profiles.

In this episode, Alison Shimada, head of the Total Emerging Markets Equity team at Allspring, and Joseph Dore, head of International Consultant Relations, discuss the strategic case for investing in emerging market equities.

Ann Miletti, Bryant VanCronkhite, and Megan Miller provide their perspectives on equity investing in 2024 and share the equity environment and opportunities they expect to see.

Taking time to sort through all the noise around artificial intelligence (AI) can uncover the quiet: promising companies with strong potential to benefit from their access to quality data.

As an accountant and auditor, Bryant VanCronkhite looked for hidden risk around every corner. Today, that risk mindset is the foundation for his team’s approach to adding value to equity strategies.

Megan Miller, head of Systematic Options, is living proof that investment in interns can yield big returns. Read about Megan and her views on the options market in this issue of PM Spotlight.

Three of Allspring’s equity leaders identify trends they believe will be evident as well as potential risks and opportunities for equity investors in the second half of 2023.