Macro Matters: U.S. Rate Cuts Coming—How Many and How Much?

Macro Matters provides a concise, comprehensive look at macroeconomic themes that matter to clients.

Key takeaways

- Growth: Global growth is stabilizing while U.S. growth is expected to continue weakening.

- Inflation: While U.S. core inflation remains sticky, we believe weakening U.S. labor market data support Federal Reserve (Fed) action.

- Rates: We expect the Fed to cut rates by 50 basis points by year-end.

Growth: Fiscal stimulus might partly offset tariff uncertainty.

Investor and consumer surveys indicate that confidence is stabilizing following the initial tariff agreements, and consumers’ spending and income remain robust. However, the latest nonfarm payroll numbers confirmed a weakening trend in hiring, and we expect more uncertainty given the slowing labor market and rising delinquencies in credit card, auto, and student loan payments.

Regarding U.S. tariffs, we’ve seen some further progress with Europe and on sectoral tariffs, and talks with China have continued. Many details are missing, though, and we believe more sectoral tariffs are likely. Beyond tariff concerns, uncertainty could increase if the U.S. government either begins taking a share of export revenue (as agreed upon with Nvidia Corp.) or a direct ownership stake (as it’s done with Intel Corp.), resulting in implicit export controls.

In the eurozone, survey data on both services and manufacturing were better than expected. Overall growth is still low, although the labor market is stable and real incomes remain robust. The tariff agreement with the U.S. has achieved, at least for the short term, some certainty for companies planning future investments. The European Central Bank (ECB) paused on rate changes for now—with wage negotiations still settling higher than preferred—but this is a lagging indicator. With lower prices, we would expect wage settlements to normalize further.

China’s growth continues to heavily rely on exports. The latest retail sales numbers confirm that lower rates and fiscal stimulus have not moved China’s consumers into a spending mood. Pressure on the property market continues—year-over-year property investments are still negative. The focus remains on boosting domestic consumption and diversifying exports away from the U.S. to other Asian countries and Europe. We believe more stimulus is needed.

Inflation: Core inflation remains elevated.

U.S. core inflation ticked up slightly in July, from 2.9% to 3.1%. Pressure generally broadened on core prices (goods and services excluding food and energy), while moderating costs in the shelter sector partly offset some of the increase. Goods inflation has risen lately, largely due to announced tariffs. Market-based inflation expectations continue to increase, while consumers’ one-year-ahead expectations declined from June’s 5.0% to 4.4% in July. However, input cost indicators, such as the Institute for Supply Management Prices Index, remain elevated, suggesting potential pass-through risks. With tariff negotiations making progress, some stabilization is likely in the coming months. In terms of further interest rate cuts, Fed Chair Powell has reiterated a cautious stance that balances inflation control with signs of softening growth.

In the eurozone, inflation continues to hover around the ECB’s 2.0% target, supported by a stronger euro. The ECB has paused its interest-rate-cutting cycle to assess the effect of year-to-date cuts on economic growth. Survey indicators have improved and wages continue to grow above target, which will likely make the ECB feel comfortable staying on hold.

In China, prices remain very low, with headline inflation dropping back to 0% year over year. The country remains in deflation, reflecting weak domestic demand and persistent property sector slowdown.

Rates: The Fed will likely restart its cutting cycle with a 25-bp cut.

The Fed is expected to cut interest rates in September, moving the federal funds rate to 4.00–4.25%. Consumer and producer price data for July continued above trend, but growth has weakened enough to provide some slight relief. Fed Chair Powell mentioned the possibility of a rate cut in his August 22 speech in Jackson Hole, Wyoming. Although the U.S. government’s pressure on the Fed to cut rates is rising, we expect that Fed members will stay focused on fundamentals despite the media attention. Weaker growth is likely to outweigh sticky inflation over the longer term. We expect two rate cuts this year to modestly support U.S. growth.

In the eurozone, the ECB has cut rates by 2.00% since early 2024, bringing the deposit rate to 2.00%. While it’s on pause, the ECB is assessing how much support the latest cuts provide. The market expects one more cut by year-end, which looks realistic to us as uncertainty around U.S. trade policies persists. The Bank of England (BoE) has reduced rates from a peak of 5.25% to the current 4.00%, with markets pricing out more cuts given sticky prices and higher-than-expected government spending. U.K. inflation trended up to 3.8% over the summer, so the BoE is likely to proceed very cautiously in order to support growth.

We expect the People’s Bank of China to continue easing to counter deflation and weak domestic demand. With China’s Consumer Price Index at +0%, further rate cuts and targeted lending programs could support growth and stabilize the property sector. Tariff negotiations are ongoing. While some kind of agreement will be found, pressure will persist on China to rebalance its economy.

Implications for fixed income

While progress has been made in tariff negotiations, bond markets will be increasingly focusing on fundamentals and on how fiscal stimulus and higher interest rates will affect growth and inflation. In the U.S., growth is likely to slow further as businesses and consumers remain cautious. Yields remain attractive overall, while international central banks are likely to be on hold for now to assess the effects of recent rate cuts.

We believe U.S. bonds will remain range-bound and earn the carry. Fiscal stimulus and a weaker U.S. dollar could lead to more volatility in longer-maturity bonds while short- to medium-term bonds remain attractive. We favor higher-quality U.S. bonds with low- to medium-term durations that are less affected by interest rate and growth volatility.

International bonds remain supported by low growth and inflation. For now, we remain positive on international bonds given stronger currencies and positive inflation developments.

Implications for equities

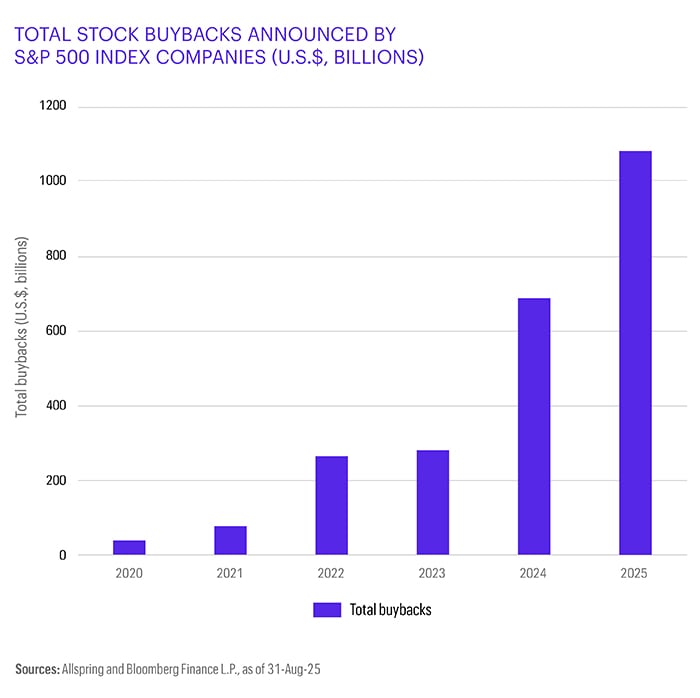

We remain modestly positive on equities overall—primarily emerging markets and cheaper sectors of the U.S. market. Earnings revisions remain positive, and while Nvidia’s earnings pointed to a more cautious outlook, the structural demand for artificial intelligence investments remains in place. Share buybacks by U.S. companies—which increase the value of remaining shares for existing shareholders—have been increasing above $1 trillion this year, as shown in the chart below (using companies within the S&P 500 Index). We see tariff negotiations having a strong impact at the sector level, although overall earnings growth is expected to remain robust. Fiscal and renewed monetary stimulus should provide further support into year-end.

We expect global equity markets to continue to perform mildly positively—including emerging markets—supported by lower real rates, stable earnings momentum, and better confidence after initial tariff settlements. Focusing on quality and valuation remains a prudent approach for us.

Implications for multi-asset portfolios

From a multi-asset perspective, we maintain a constructive view on global equities, particularly in emerging markets and China, where valuations remain attractive and trade sentiment has begun improving. Within the U.S., we prefer sectors less affected by tariffs, like information technology. On a relative basis, we’ve started adding back to U.S. equities over other developed market nations. We expect the Fed’s eventual pivot toward growth support to bolster equity sentiment further. Robust share buybacks should provide further support to equities.

We continue to like medium-term maturity bonds over cash. In the U.S., we believe the interest rate curve has room to steepen. With the Fed gradually expected to shift from inflation to growth support in the second half of 2025, U.S. equities should benefit from lower interest rates, fiscal stimulus, and waning tariff concerns. Tariffs are, however, here to stay and could potentially create short-term uncertainties through sectoral tariffs. We remain underweight the U.S. dollar given the outlook for lower interest rates in the U.S., and we prefer gold as a diversifier.

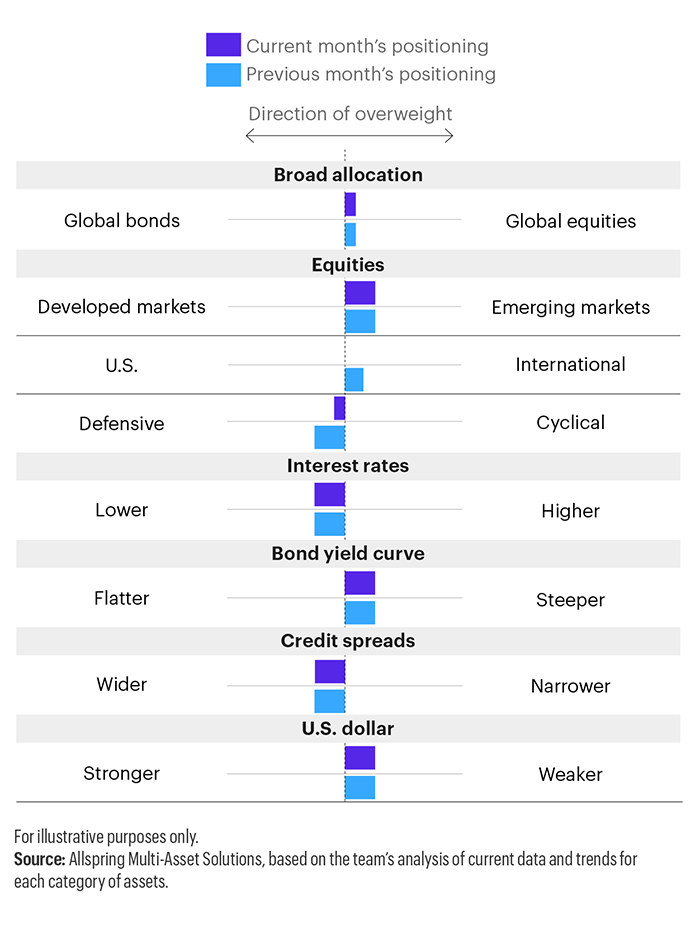

Potential allocations based on today’s environment

The table below depicts our views on short-term trends. These perspectives are developed using quantitative analysis of data over the past 30 years overlaid with qualitative analysis by Allspring investment professionals. The positioning of each bar in the table shows the direction and magnitude of an overweight.

100 basis points (bps) = 1.00%

This material is provided for informational purposes only and is intended for retail public distribution in the United States. Use outside the United States is for professional/qualified investors only.

ALL-09082025-zya1ngcl

Related insights

Which macroeconomic trends do we think matter the most? Read through the investment implications in this month’s issue of Macro Matters.

The Federal Reserve (Fed) once again held rates steady against a mixed backdrop of elevated inflation, a weaker labor market, and stable growth (for now). Amid rising geopolitical risk, time will tell how U.S. fundamentals are affected.

Which macroeconomic trends do we think matter the most? Read through the investment implications in this month’s issue of Macro Matters.

Article

Market Impacts: Iran ConflictJoint U.S.-Israeli attacks on Iran over the weekend have sparked a conflict that could draw in much of the Middle East. Explore the short- and long-term implications for investors.

Which macroeconomic trends do we think matter the most? Read through the investment implications in this month’s issue of Macro Matters.

The Federal Reserve (Fed) held rates steady amid solid growth and sticky inflation, with markets reassessing rate-cut expectations as rising commodities, a weaker USD, and political uncertainty complicate the outlook.

Article

Macro Matters: Carry OnWhich macroeconomic trends do we think matter the most? Read through the investment implications in this month’s issue of Macro Matters.

Venezuela's political transition sparks global market ripples, boosting gold and the U.S. dollar while raising questions about oil production, regional politics, and global power dynamics. Explore the short- and long-term implications for investors.

Article

A Fine BalanceThe Federal Open Market Committee (FOMC) dropped its key interest rate by 0.25% to 3.50–3.75%. Going into 2026, we see signs that fiscal stimulus will be more meaningful in addressing the current weakening labor market.

Allspring PMs keep their fingers on the pulse of the markets—and their selfie cameras—going into 2026.

George Bory and Ann Miletti share Allspring's 2026 outlook. From resilient bond strategies to AI-powered equity growth, they unpack the key drivers set to shape next year's financial markets.

Which macroeconomic trends do we think matter the most? Read this month’s issue of Macro Matters.

Article

Nothing to See HereDespite limited access to reliable data due to the ongoing government shutdown, the Federal Open Market Committee (FOMC) announced another 0.25% cut, lowering its key interest rate to 3.75–4.00%.

How are Allspring’s investment experts thinking about the U.S. government shutdown and market implications?

Macro Matters provides a concise, comprehensive look at macroeconomic themes that matter to clients.

The Federal Reserve lowered its key rate by 25 basis points at its September meeting following an eight-month pause. George Bory and John Campbell discuss how U.S. bond and equity markets could respond.

Macro Matters provides a concise, comprehensive look at macroeconomic themes that matter to clients.

With a robust U.S. economy, above-target inflation, and continued tariff uncertainty, the FOMC kept its key interest rate at 4.25–4.50%.

Macro Matters provides a concise, comprehensive look at macroeconomic themes that matter to clients.

Speculation over the next chair of the Federal Reserve (Fed) is dominating headlines and keeping markets on edge. A more dovish leader could mean a big shift in monetary policy and raise concerns about the Fed’s independence.

As the events concerning Iran continue, Allspring Fixed Income’s message—"bonds provide certainty in an uncertain world”—remains central to our positioning.

A potential conflict with Iran has consistently appeared in our monthly Market Risk Monitor for over two years. Now that risk has materialized. Our equity portfolio managers assess the implications for global markets.

What might the future hold for markets? In this roundtable discussion, our investment experts explore pressing topics like deficit spending, trade tensions, the Fed’s next moves, and the weakening U.S. dollar.

With ongoing tariff uncertainty and U.S. employment still strong, the Fed kept its key interest rate at 4.25–4.50%.