Capabilities

Fixed Income Investment Approach

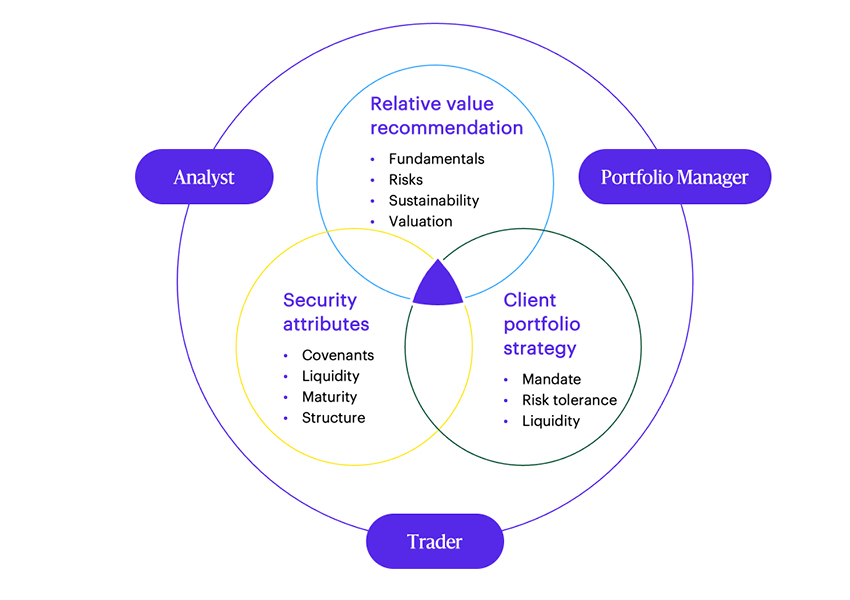

We build portfolios from the bottom up, security by security

Our proven investment approach to fixed income portfolio management is grounded in the combination of deep fundamental research and risk-controlled portfolio construction.

This enables our portfolio managers to drive performance primarily through security selection while exercising independent portfolio positioning to manage macro risks.

We believe our fixed income platform encourages the seamless exchange of best ideas and practices that enables us to manage prudently through changing economic cycles.

Fixed income is a core strength, with $485 billion in assets under advisement*

Offering a wide range of fixed income investment capabilities

*Allspring and affiliates. Figures are as of December 31, 2025, unless otherwise noted. Please note that the assets under advisement (AUA) figures provided include discretionary and non-discretionary assets and have been adjusted to eliminate any duplication of reporting among assets directed by multiple investment teams and includes $81B from Galliard Capital Management ($60B stable value; $21B fixed income). AUA includes non-discretionary assets that are not captured in Allspring’s assets under management (AUM) figure of $558B, which includes Galliard, an investment advisor that is not part of the Allspring trade name/GIPS firm.

Bonds are once again becoming cornerstone of portfolio allocations expected to generate steady, predictable returns over the coming months and years.

George Bory, Chief Investment Strategist – Fixed Income

Driving performance through security selection

Our fully integrated investment process seeks to identify and capture the most attractive risk-adjusted investments for client portfolios.

We offer a wide array of fixed income solutions across the duration term structure and risk spectrum of global bond markets, driven by deep fundamental research from our Global Fixed Income Research team.

Jon Baranko, Chief Investment Officer – Fundamental Investments

Deep fundamental credit research capabilities

Our fixed income platform offers solutions across asset classes and around the world that are supported by deep fundamental credit research capabilities.

- Large, experienced team of sector specialists

The team's extensive knowledge of industry nuances enables timely and informed decision-making. - Broad, diverse coverage universe

U.S.- and European-based analysts bring invaluable local knowledge and insight to the process. - Relative value focused recommendations grounded in fundamental analysis

This enables portfolio managers to weigh factors affecting the credit and to seek to add value to portfolios. - Focused assessment of sustainable and climate transition risk factors enhances fundamental research

Risks can stem from these factors, but also from regulation and consumer preference, which can materially affect companies and sectors. - Seamless flow of information promotes collaboration

This ensures securities are thoroughly vetted via multiple viewpoints by leveraging our global scale and footprint.

Fixed income leader

Chief investment officer

Lead portfolio managers

Featured insights

Nick Venditti, Allspring’s head of Municipal Fixed Income, explains the impact of the recently passed One, Big, Beautiful Bill on our SpringTalk Muni Moments. And the good news for muni investors? It’s not bad news.

Allspring's Plus Fixed Income team explains the three key elements they believe may lead to a more balanced and enhanced return profile.